When Your Business Dies With You

The Estate Planning Crisis Every Entrepreneur Ignores

The Hidden Truths series Post 02

The Hidden Truths examines the gap between what families believe their estate plan will do and what the legal system actually does after a death. Each post follows one family through one specific failure that planning could have prevented.

At 3:47 in the morning on a Tuesday, Jennifer’s phone buzzed on the nightstand.

“Dad’s in the hospital. Heart attack. Come now.”

By the time she arrived, her father was gone. Tom was fifty-four years old. He had spent two decades building a real estate practice in Phoenix: 800 clients, $200,000 in annual income, fifteen pending transactions worth $50,000 in commissions, and a referral network he had cultivated relationship by relationship over twenty years.

Within forty-eight hours, all of it was gone.

Not because Tom had done anything wrong. Not because the business was fragile or poorly run. Because a real estate license in Arizona expires at death. Because the client database was locked behind accounts only Tom had access to. Because the pending transactions had no legal mechanism to continue without the licensed agent who originated them. Because twenty years of professional relationships existed between Tom and his clients, and Tom was no longer there.

Jennifer and her family did not inherit a business. They inherited the absence of one.

Most people understand, in a general way, that estate planning matters. They have heard the arguments about wills and trusts and guardians and probate. What most people do not understand, and what catches business-owning families completely unprepared, is that a business is a fundamentally different kind of asset than a house or a retirement account or a life insurance policy.

A house has a deed. It transfers through a documented legal mechanism whether or not the owner planned for it. A retirement account has a beneficiary designation. A life insurance policy pays out to whoever was named. These assets were designed to survive their owners because the systems that hold them were built with transfer in mind.

A business was built to generate income for the person running it. When that person dies, the income stops. The clients look elsewhere. The licenses expire. The accounts freeze. The contracts lapse. The relationships, which were personal to the owner, do not transfer to anyone because there is no mechanism to transfer them. A business without a succession plan does not pass to the next generation. It simply ends.

Tom’s family had assumed, as most families do, that the business would be part of what he left behind. It was his largest asset. It represented more than the house, more than the savings, more than the life insurance payout. And it was the only thing that produced nothing when he died.

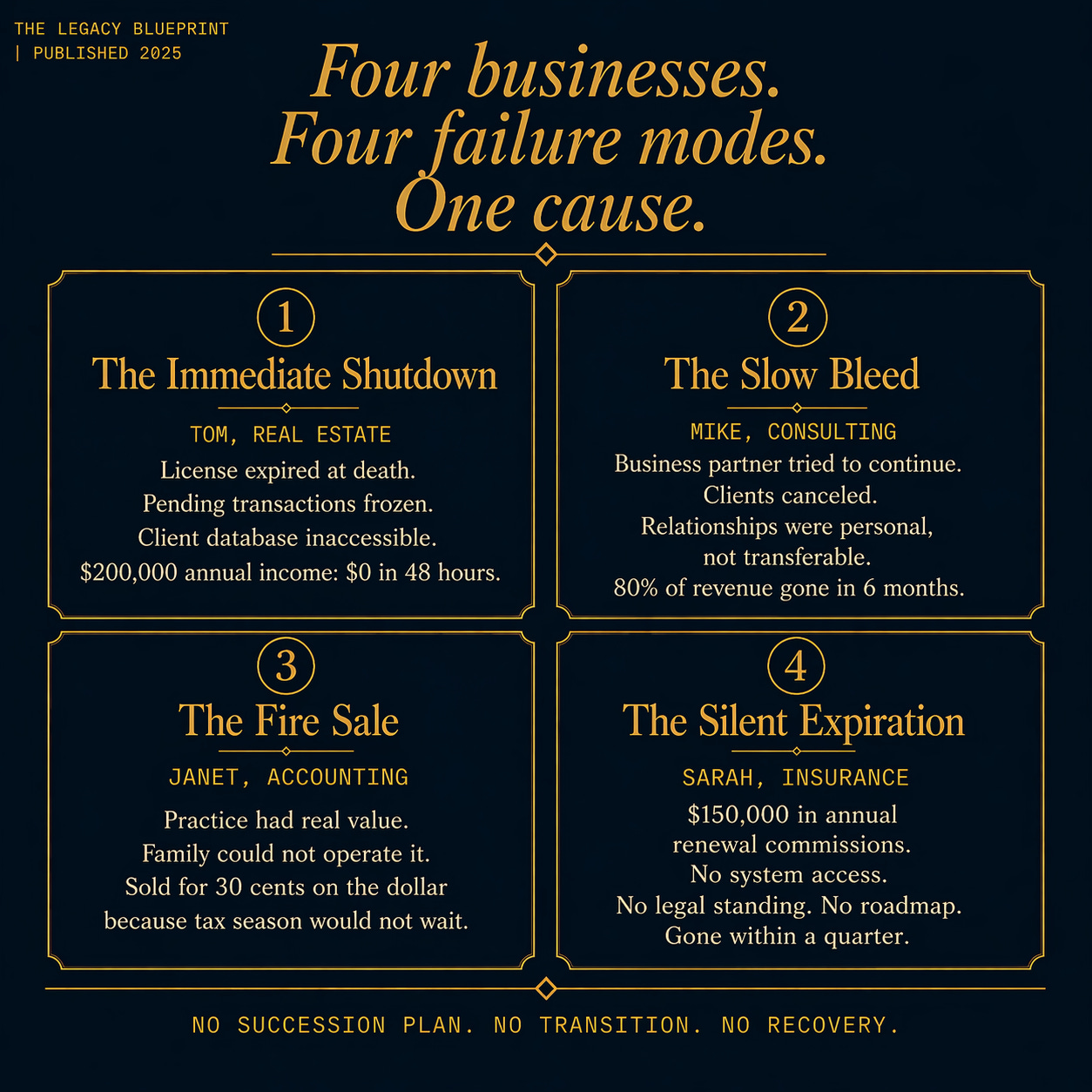

Tom’s story is the version that happens in forty-eight hours. The business vanishes immediately because the license expires and the accounts lock and there is no legal structure to keep anything operating for even a week. But there are other versions, and they take longer, and in some ways they are harder to watch.

Sarah was an insurance agent whose renewal commissions generated $150,000 a year. When she died suddenly, her husband could not access her client management system, did not know which policies were coming up for renewal, and could not legally represent her clients even if he had known what to do. He was not incompetent. He simply had no legal standing, no system access, and no roadmap. The renewal commissions that would have continued paying the family for years evaporated inside of a quarter.

Mike ran a consulting business with $300,000 in annual contracts. He had a business partner, which most people assume is a form of protection. The partner tried to continue the work after Mike died. The clients started canceling. Not because the partner was doing a poor job, but because the clients had hired Mike. They had relationships with Mike personally. The contracts were structured around Mike’s specific involvement. Within six months, eighty percent of the revenue was gone because there was no transition plan that could have redirected those relationships to someone else while they were still warm.

Janet’s family faced a different problem. Her accounting practice had genuine market value: an established client base, recurring annual engagements, a reputation that had taken decades to build. The family could not operate it and needed income. Tax season was approaching. They sold for thirty cents on the dollar because the buyer understood the urgency and priced accordingly. The practice that represented Janet’s life’s work sold for a fraction of what it was worth because there was no time and no plan.

Four businesses. Four different failure mechanisms. The same root cause in every case.

The specific failure mode depends on the type of business. But the underlying problem is consistent across all of them: a business that exists because of one person’s relationships, licenses, expertise, and access does not survive that person’s death without deliberate preparation.

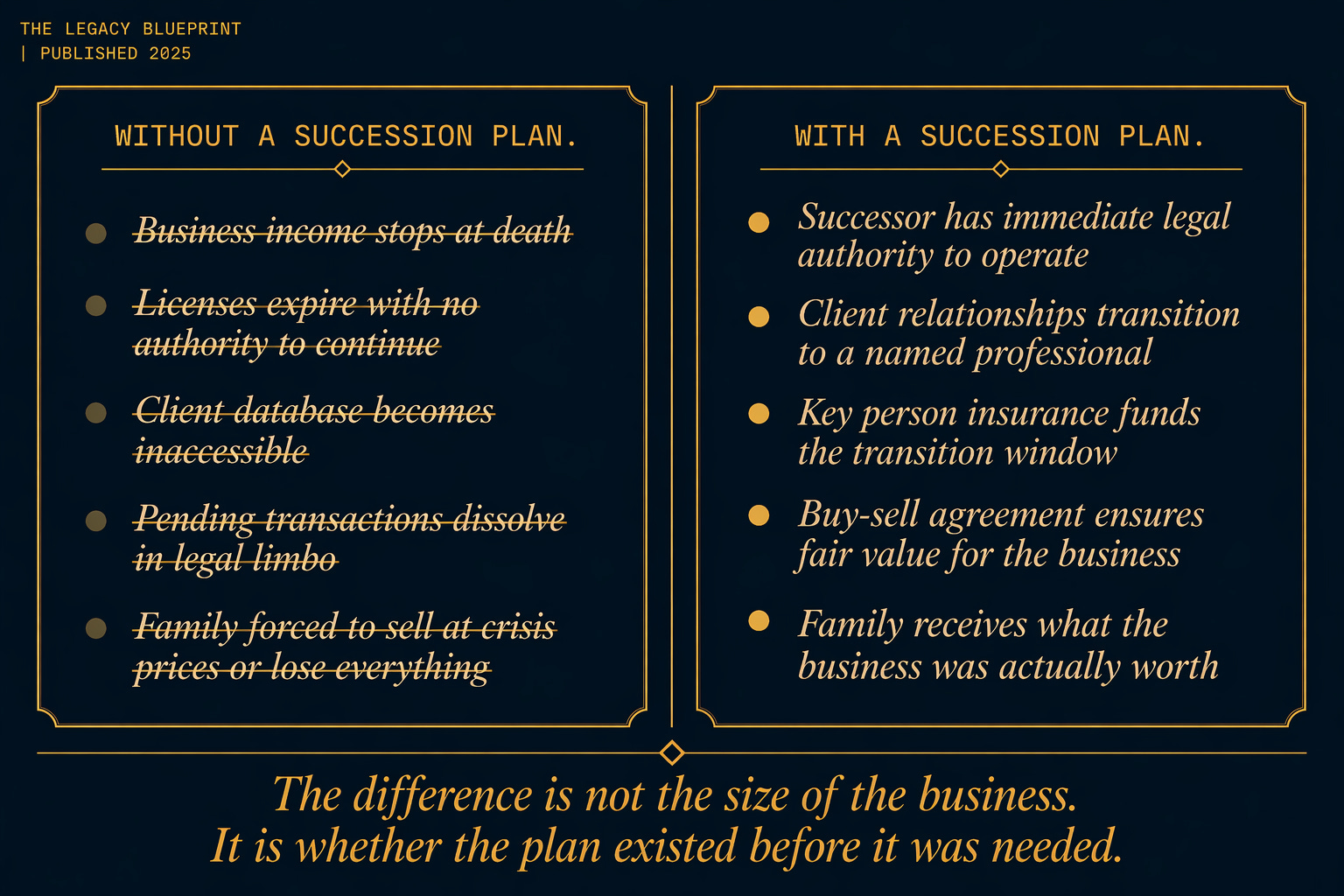

The preparation is not complicated in concept. It is specific in execution, and it requires being done while the owner is alive and capable of making decisions.

A succession plan for a solo practitioner or solopreneur typically addresses several things simultaneously. It establishes who has legal authority to access accounts and systems in the immediate aftermath of the owner’s death. It documents client relationships with enough specificity that another professional can step in and maintain continuity. It identifies that other professional in advance, through a referral partnership or a buy-sell agreement with a peer in the same field, so there is somewhere for the clients to go that preserves the value of the relationships rather than losing them to attrition. It creates a transition window, funded by key person life insurance, that gives the business enough runway to transfer its value rather than dissolve under time pressure.

None of this is exotic. It is the application of standard estate planning logic to an asset class that most estate plans ignore entirely. A will addresses the house and the retirement accounts. A trust holds the investment portfolio. The business, which is often the family’s largest single asset, gets a paragraph in the will that says nothing useful about how to operate, transfer, or sell it.

Jennifer spent four months after Tom’s death trying to recover something from the business he had built. She contacted his clients. Most of them had already moved to other agents, which was the rational thing to do since their transactions needed to close and Tom was no longer available. She found an attorney who specialized in real estate business transitions and was told, politely, that there was not much to transition. The license was gone. The pending deals had been redistributed. The database had value in theory but no mechanism to monetize it without a license.

Tom had talked about getting things organized. He had mentioned, more than once, that he should meet with an estate planning attorney about the business. He had thought about who might be a logical successor among the younger agents in his network. He had just not gotten around to formalizing any of it.

He was fifty-four. It did not feel urgent.

Arizona has specific tools that make business succession planning more effective here than in most states. The state’s business-friendly legal framework allows for trust structures that can hold business assets and continue operations after the owner’s death. Buy-sell agreements can be structured in advance between professionals in the same field, with the purchase price funded by life insurance, so that the surviving family receives market value for the business without needing to find a buyer under time pressure. Key person insurance policies can fund the transition period, covering business expenses and giving a successor professional enough runway to earn the trust of the existing client base.

These tools do not work unless they are set up while the business owner is alive, in good health, and able to make decisions. The buy-sell agreement requires a counterparty who is willing to enter it. The key person insurance policy requires the business owner to be insurable. The succession documentation requires the business owner to have the mental clarity and the time to produce it accurately.

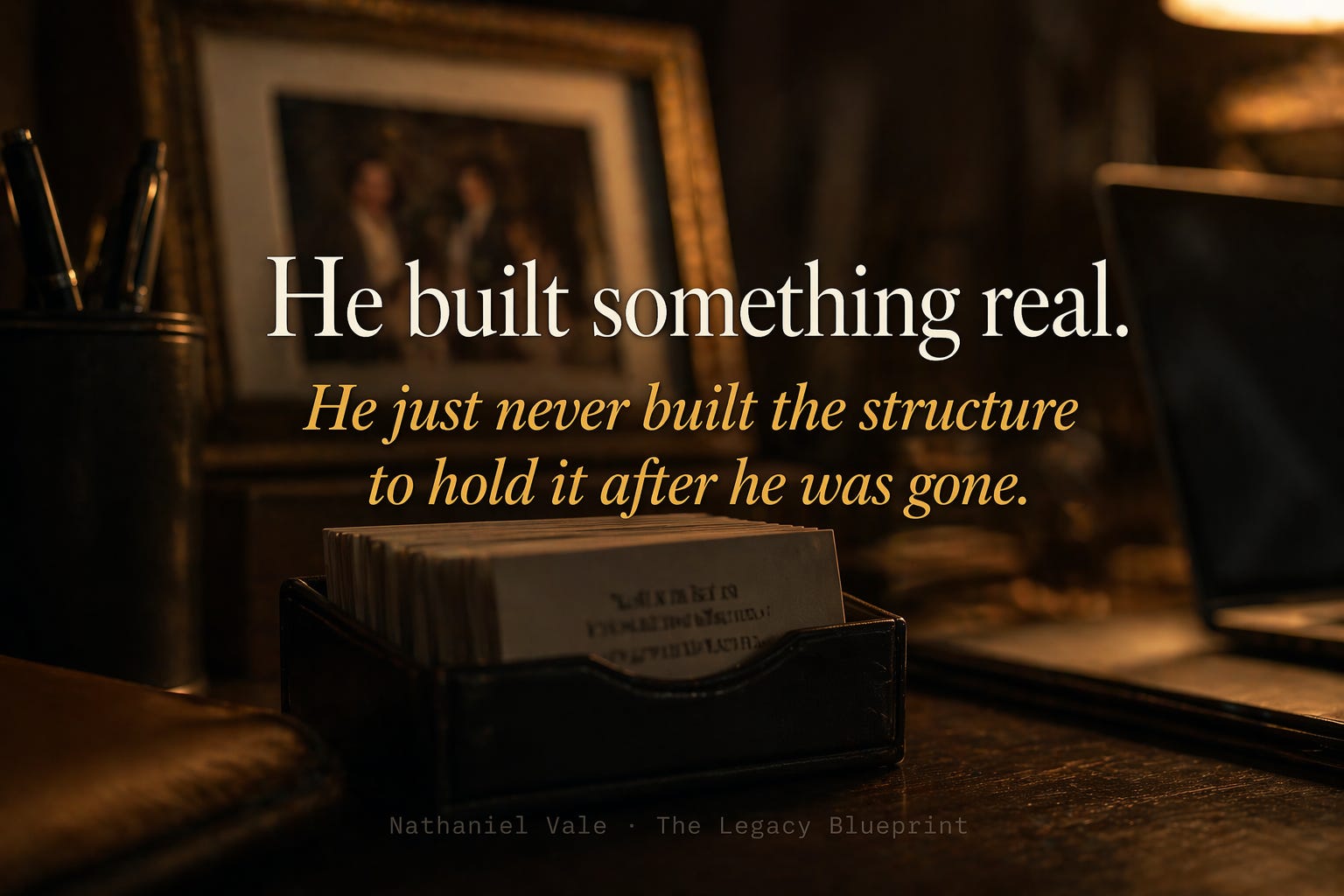

Tom had all of those things. For twenty years, he had the time, the health, the relationships, and the capacity to build a succession plan that would have protected what he built. He simply did not get around to it.

Jennifer still lives in Phoenix. She works in corporate real estate now, a stable job with a salary and benefits. The transition from her father’s sudden death to financial stability took almost two years.

Tom’s client database, the 800 relationships he had built across twenty years, is scattered across a dozen different agencies now. The clients found other agents. That is how it works when there is no plan: the business does not transfer. It disperses.

He built something real. He just never built the structure to hold it after he was gone.

Among the families I work with, the ones who own businesses face the highest-stakes version of the estate planning gap, because a house that goes through probate loses time and money, while a business that goes through probate without a succession plan may not survive the process at all.

The masterclass covers what business succession planning actually looks like for solo practitioners and small business owners; what documents are needed, how buy-sell agreements work, what key person insurance covers, and what specific steps protect a business from becoming the kind of story this post describes.

The Estate Planning Blueprint Masterclass is a free one-hour class for families who want to build an estate plan that holds up. It walks through the three things every plan needs to keep probate out, protect children from avoidable conflict, and pass wealth to the next generation cleanly. Readers who recognized the patterns in this post and want to start building the structure that prevents them can register here:

Register for the Masterclass

Readers who would prefer to discuss a specific situation directly can book a free consultation here:

https://lastinglegacypro.com/estate-planning

Nathaniel Vale / The Legacy Blueprint