They Taught You the Definitions. Nobody Taught You the System.

An introduction to Financial Literacy Basics

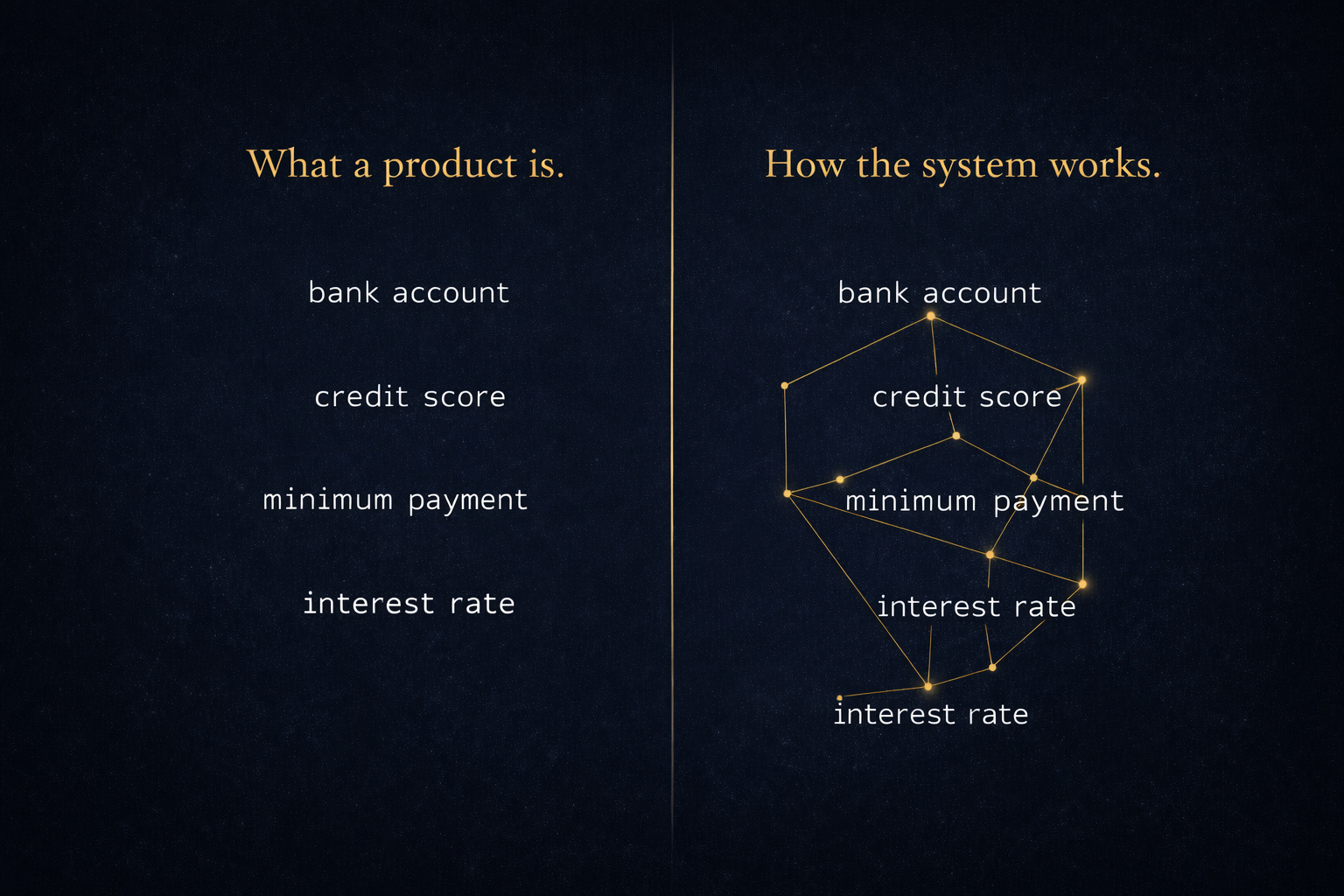

At some point, someone explained to a family what a bank account was. What a credit score was. What interest meant, roughly. What a minimum payment was and where to find it on a statement.

And then that family went out and used those products for decades, losing ground the entire time, with no clear explanation for why.

The definitions were accurate. The products were real. The system those products operated inside was never mentioned.

That gap is not an accident. It is the natural result of a financial education designed around instruments rather than architecture. Knowing what a bank account is tells a household nothing about how the banking system generates revenue from the people using it. Knowing what a credit score is tells a household nothing about who built the scoring model, who benefits from its structure, or what a 50-point gap costs over 30 years of borrowing. Knowing what a minimum payment is tells a household nothing about why it is engineered the way it is, or what the person making that payment is actually producing for the institution on the other side of it.

Definitions describe the tool. Nobody handed anyone a map of the terrain the tool operates inside.

That is what this series is for.

Every financial product a household uses was designed by someone, for a specific purpose, with specific beneficiaries in mind. The beneficiary is not always the user.

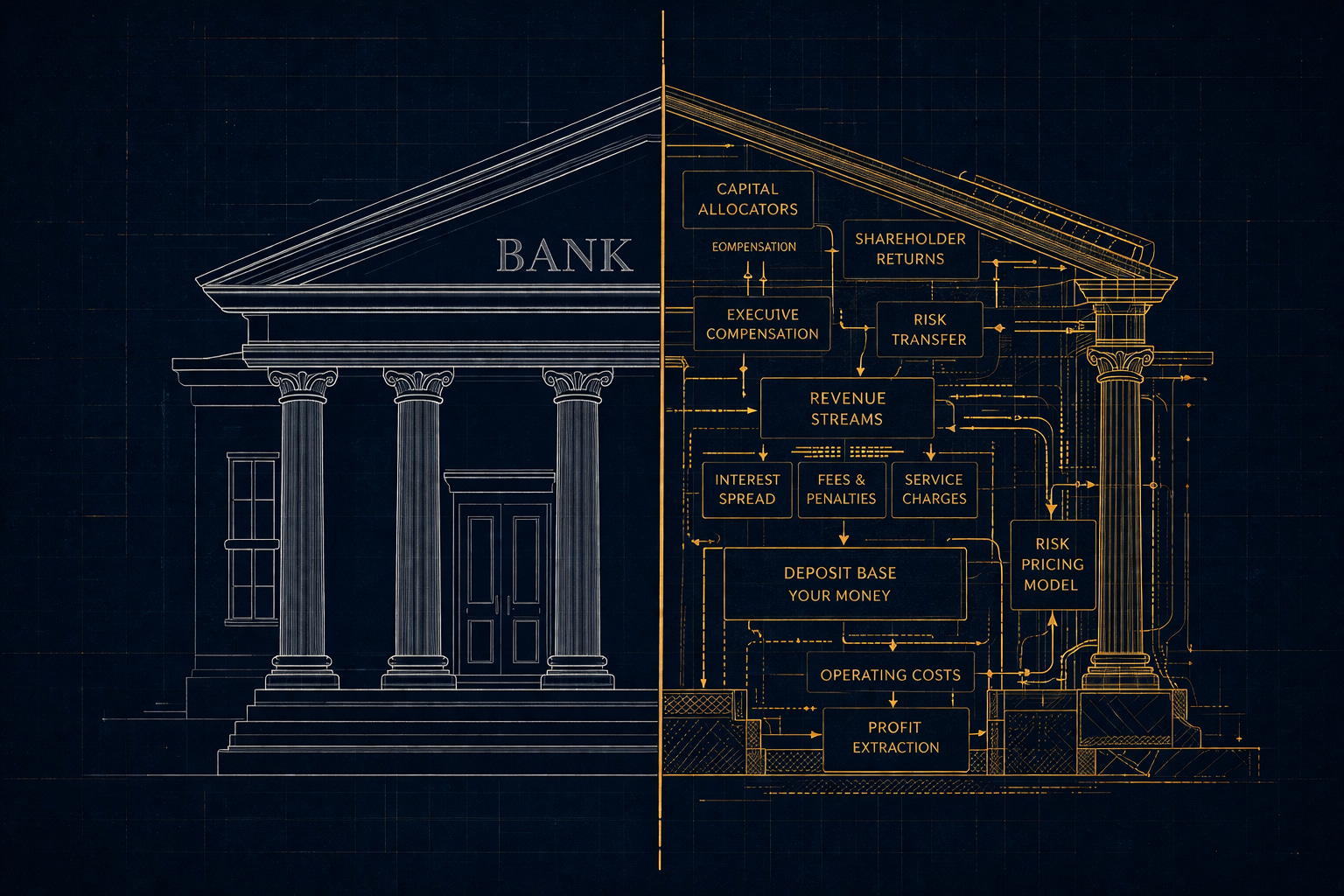

The overdraft fee was not designed as a consumer protection feature. The minimum payment structure was not designed to help families get out of debt faster. The credit reporting model was not built by a neutral party with no stake in the outcome. These are systems with architectures, and those architectures produce predictable results whether the person inside them understands what is happening or not.

This is the core argument behind the Financial Literacy Basics series. Financial instability is not primarily caused by low income or poor character. It is caused by the absence of a working model — a frame for understanding how the systems a household already uses every day actually function, who they serve, and what they cost when operated without that understanding.

Most families are not losing ground because they are irresponsible. They are losing ground because they are operating infrastructure they were never taught to read.

The Financial Literacy Basics series is three books. Each one builds on the last.

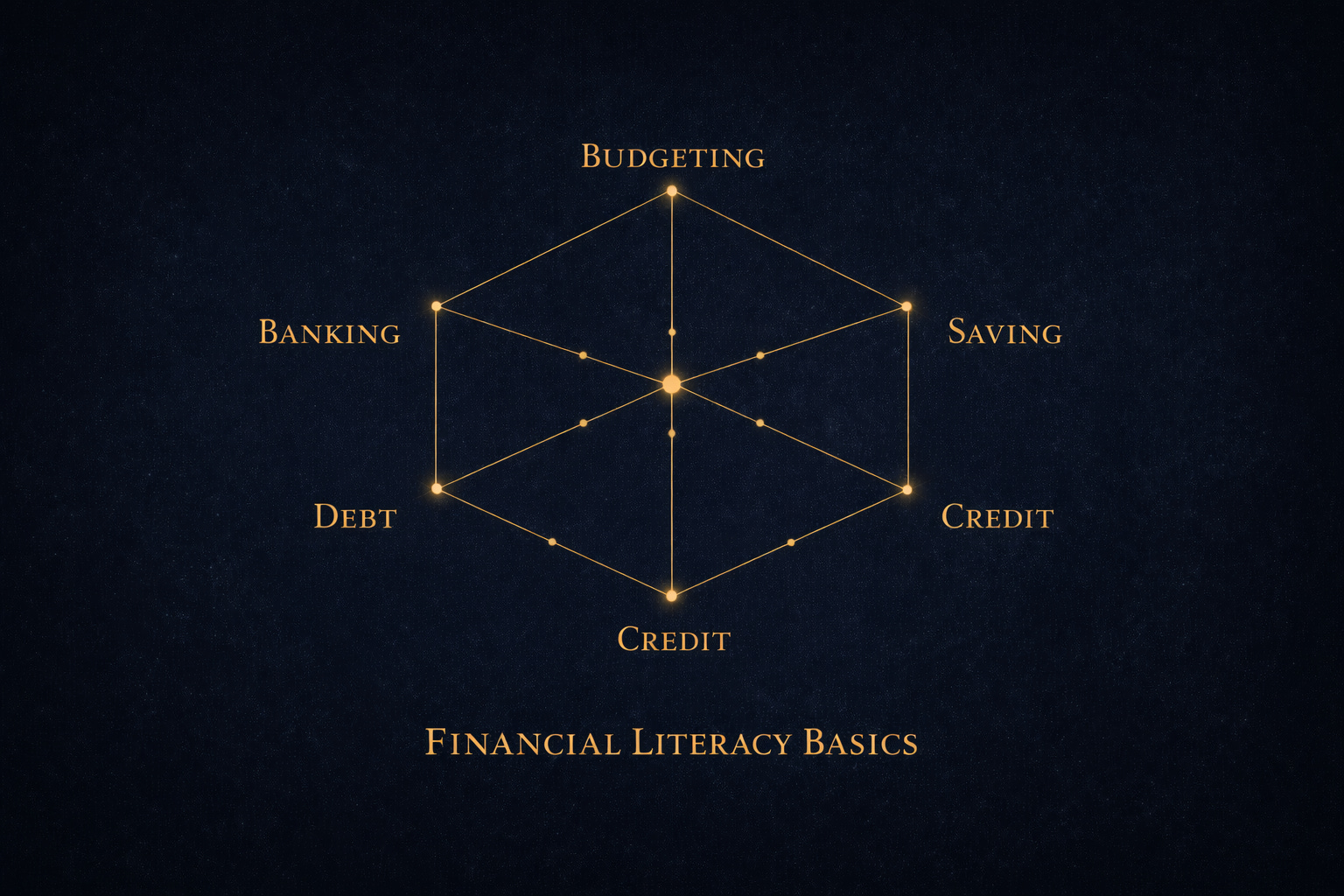

The first book, Core Money Skills, covers the five foundational systems every household touches regardless of income level: budgeting, banking, saving, debt, and credit. It does not cover every banking product or walk through every debt instrument in existence. What it covers is how each of these systems works, what it was designed to do, and what changes when a family understands the full picture before making decisions inside it.

That principle matters more than it might appear. A household that understands how the banking system generates revenue can navigate any specific banking product without a separate lesson for each one. A household that understands how credit scoring functions can evaluate any new credit product against that framework. The goal is not a library of definitions. The goal is a working model that transfers.

The second book, Protect and Grow Wealth, shifts from defense to offense. Once the foundation is stable, the focus moves to building and protecting what has been earned — investing, taxes, insurance, financial goal structures — the same analytical approach applied to a different set of systems.

The third book, Wealth and Innovation, expands the frame to generational thinking. Estate planning, legacy structures, financial technology, entrepreneurship as an income system. The question that book answers is not how to get stable, but how to make sure stability compounds across generations rather than resetting with each one.

Here is the framing most financial content will not say directly.

Every financial system a household uses was built by someone with a business model. The banking system profits from fee revenue and the spread between what it pays depositors and what it charges borrowers. The debt industry profits from time-in-debt. The credit industry profits from the complexity and information asymmetry it creates. This is not a conspiracy. It is how those businesses operate.

Inside that structure, households are either the party that understands the system or the party the system was designed to extract from. There is no neutral position. A household that does not understand how the minimum payment on a credit card is structured will produce a predictable outcome for the institution holding that card, regardless of what that household intends.

The language of predator and prey is not melodramatic. It is accurate. Most people absorb the prey position not because they chose it, but because no one handed them a map of the terrain before they started crossing it.

This series is the map.

Financial literacy, properly understood, is not a vocabulary test. It is the capacity to look at a financial system, understand what it was designed to do, identify where household interests and institutional interests diverge, and make decisions accordingly.

That capacity does not require a finance degree. It does not require high income or prior exposure. It requires a working model of how these systems function, delivered in a sequence that builds understanding rather than cataloging terms.

There is one thing this series is built to deliver above everything else: a reader who finishes all three books will never again encounter a financial product, a financial decision, or a financial institution and wonder how it actually works. The architecture will be visible. The incentive structure will be legible. The decision will belong to the household, not to whoever designed the system it is operating inside.

That is not a guarantee of wealth. It is something more durable: the permanent removal of a specific kind of disadvantage.

Three books. Five foundational systems in the first one. A framework that transfers across every financial product that will ever be encountered. And enough clarity about how these systems actually operate that the next generation does not have to start from zero.

The first book is already written. The work starts here.

Nathaniel Vale is the author of Core Money Skills, Book I of the Financial Literacy Basics series, part of the Generational Wealth Engine.