The Probate Nightmare That Could Have Been Avoided

How the Absence of a Plan Cost One Arizona Family 847 Days, $80,000, and the Life They Were Supposed to Have After

The Hidden Truths series Post 06

The Hidden Truths examines the gap between what families believe their estate plan will do and what the legal system actually does after a death. Each post follows one family through one specific failure that planning could have prevented.

Two weeks after Robert’s funeral, Carol walked into their bank.

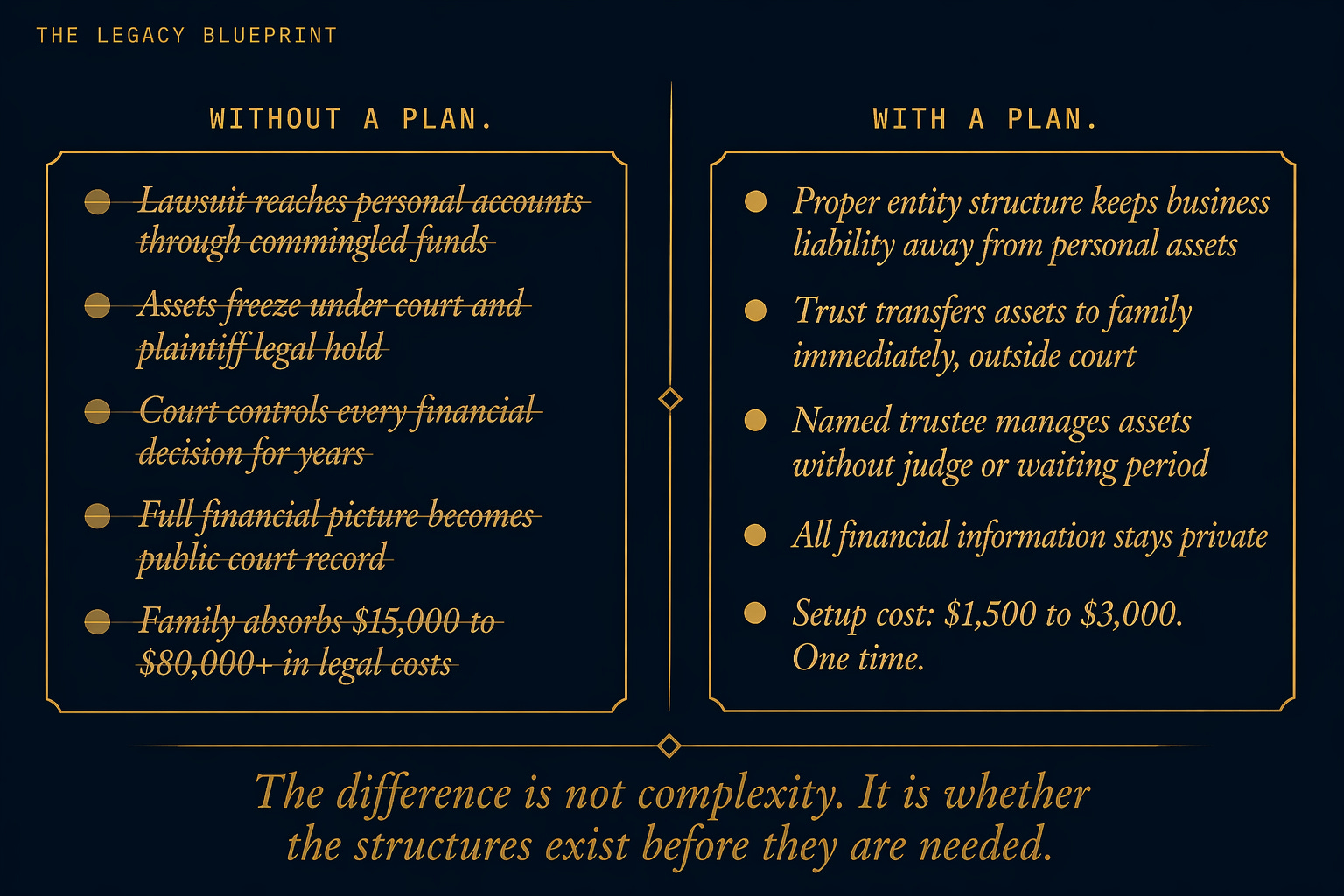

She had been a joint account holder for thirty-one years. She knew the branch manager by name. She brought the death certificate, the marriage certificate, and every document she thought might be needed. What she did not expect was the phone call the branch manager made while she sat across the desk. A legal hold had been placed on the accounts. Not by the court. By the attorneys representing the plaintiff in a lawsuit against Robert’s business. The hold asserted that funds in the personal accounts had been commingled with business assets and were subject to the damages claim.

The branch manager was apologetic. There was nothing he could do.

Carol drove home without the money she needed to pay the mortgage due in eleven days, trying to understand how a lawsuit against Robert’s company had reached inside her personal checking account.

That was day fourteen. There were 833 more to go.

Robert had owned a small general contracting business in the Phoenix metro for eighteen years. He was good at the work, well-regarded by his clients, and had built the company steadily over two decades. Fourteen months before he died, a former client filed a lawsuit claiming defective construction on a commercial project. The case was disputed. Robert believed he would win. He hired an attorney and kept working.

What Robert had never done, in eighteen years of running a successful business, was formally separate his personal finances from his business finances. He paid personal expenses from the business account when cash flow was convenient. He deposited business income into personal accounts when timing worked better that way. It was common practice for small business owners, and it had never caused a problem. Until it did.

When the plaintiff’s attorneys began examining Robert’s finances as part of discovery, they found what commingling always produces: no clean line between what was personal and what was business. They filed to have the mixed accounts frozen pending resolution of the damages claim. The argument was straightforward: if personal and business funds were indistinguishable, all of it was potentially subject to the lawsuit.

Robert was managing the legal stress, the business, and the marriage and family he had spent thirty-two years building when he had a heart attack at fifty-nine. He died before the lawsuit was resolved. The lawsuit did not die with him.

When Robert died, two separate legal processes opened simultaneously, and Carol was at the center of both with no legal authority over either.

The first was probate. Robert had no estate plan, no trust, no transfer-on-death designations, no documented instructions of any kind. Under Arizona law, his estate entered the court process by default. A judge Carol had never met would oversee the distribution of everything Robert had built. The house, the savings, the investment accounts, the business itself: all of it frozen until the court worked through the process at its own pace.

The second was the continuation of the lawsuit. The business entity did not cease to exist because its owner died. The plaintiff still had a claim. The plaintiff’s attorneys still had a legal hold on accounts they argued contained commingled funds. The fact that Robert was gone did not change the damages they were seeking or the legal mechanism they had used to pursue them.

Carol was a surviving spouse in a community property state with no criminal history, no disputed claims of her own, and thirty-two years of marriage to a man who had fully intended to protect her. She could not access her accounts because a contractor’s dispute and a missing estate plan had created a legal situation that treated her finances as an open question.

The costs were not abstract.

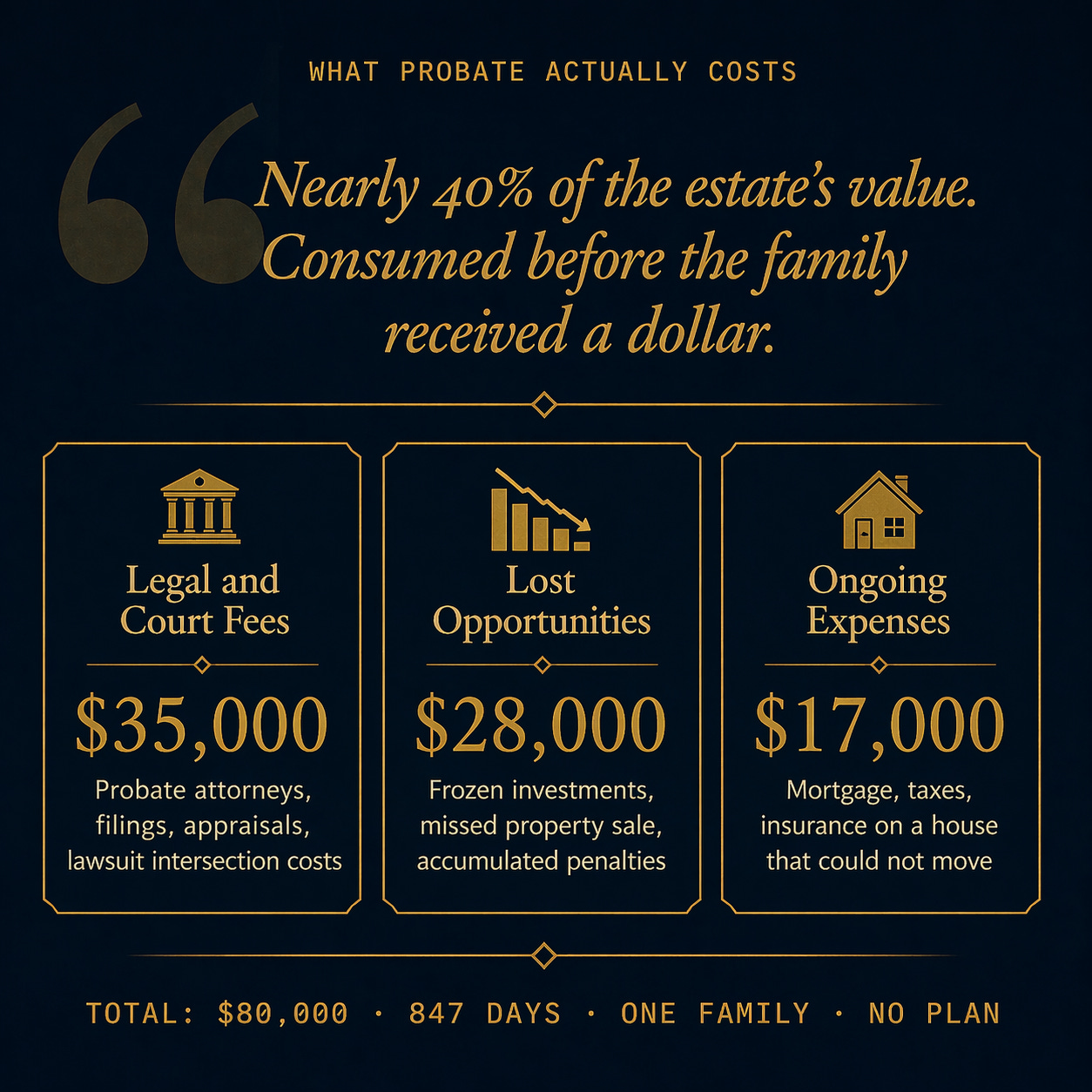

Legal and court fees consumed $35,000: probate attorneys, estate filings, asset appraisals, administrative costs, and the additional work generated by the lawsuit’s intersection with the estate. Lost opportunities added $28,000: investment accounts that deteriorated unmanaged, a property sale that could not happen when market conditions were right, credit penalties that accumulated on debts Carol could not pay from frozen funds. Ongoing expenses on frozen assets ran $17,000: mortgage payments, property taxes, insurance, and maintenance on a house that could not be sold or transferred. Total: $80,000. Nearly forty percent of the estate’s value consumed before a single dollar reached the family it was meant for.

Carol had expected to grieve. She had not expected to fight.

Her oldest son, believing she should have been able to access the accounts sooner, blamed her for the delays. He did not understand that she had no legal authority to do anything without court approval, and Carol had no bandwidth to explain it. She was appearing in court. She was managing an estate attorney she could not pay from frozen accounts. She was fielding correspondence from the plaintiff’s legal team, who did not pause the lawsuit because its defendant had died and left behind a widow.

Her youngest son left college in the second year. The money that would have covered his tuition was in accounts the court had not yet released. He told Carol he would go back when things settled down. He has not gone back.

Her daughter stopped coming home. The family gatherings that had always happened around Carol and Robert’s kitchen table became contested discussions about the estate, about the lawsuit, about what was fair and who was responsible and whether any of it could have been prevented. Then they stopped happening altogether.

Carol lost thirty pounds over the course of the proceedings. She developed anxiety severe enough to require medication. She started having panic attacks before court appearances. She entered therapy not to process the loss of her husband but to manage the legal crisis that had replaced her ability to grieve him.

Robert’s memory, in those 847 days, became inseparable from the conflict that followed his death. The family that gathered to remember him at the funeral became the family that fought over what he left behind. That is not what he would have wanted. It is not what he intended. It is simply what happens when intention meets an unprepared system.

There is another cost that does not appear on any court filing.

When Robert’s estate went through probate, everything they had built together became part of the public court record. The asset inventory, the debts, the lawsuit, the family disputes, the personal documents submitted as evidence. Anyone who walked into the Maricopa County courthouse could read it.

Carol discovered this the way most families do: from someone who had already seen it. A neighbor mentioned, in passing, that she had come across the family’s financial records in the court filings. She meant no harm. The information was simply there.

“I felt violated,” Carol said later. “Robert would have been mortified. He was an intensely private man. He worked his whole life to build something for this family, and strangers were reading about it at a courthouse counter.”

Robert’s privacy was not protected by his intentions. It was governed by the structures that existed when he died. A revocable living trust keeps a family’s financial picture out of the public record entirely because assets transfer outside the court process. Robert’s estate had no such structure. So the record was public. And Carol, who had already lost her husband and her savings and her youngest son’s college years, also lost the privacy of the life they had built together.

Robert’s story contains two distinct failures, and it is worth naming both of them.

The first is the missing estate plan. No trust, no transfer-on-death designations, no documented instructions. That failure handed the court control of everything Robert owned and gave Carol no legal authority to act on her own behalf.

The second is the missing business protection structure. Eighteen years of running a successful company without a formal separation between personal and business finances. No LLC with properly maintained separation. No asset protection structure that would have kept a lawsuit against the business from reaching Carol’s personal accounts. No buy-sell agreement that would have addressed what happened to the business when its owner died.

These are separate problems with separate solutions, and either one addressed would have changed what happened to Carol. Both unaddressed produced the outcome you have read about in this post. A future post in this series addresses the business succession failure specifically, because it deserves its own full accounting. What matters here is that the two failures are connected: a business owner who has not protected personal assets from business liability needs an estate plan that accounts for that vulnerability, and most do not have either.

Arizona has more tools for avoiding this than most states. A revocable living trust transfers assets directly to named beneficiaries without court involvement: no public record, no mandatory waiting period, no asset freeze. A transfer-on-death deed allows real estate to pass automatically at death for less than $100 to prepare. Beneficiary designations on life insurance, retirement accounts, and bank accounts move those assets outside probate entirely. And proper business entity structuring, maintained correctly from the start, keeps a lawsuit against a company from becoming a legal hold on a family’s personal accounts.

A comprehensive estate plan in Arizona costs $1,500 to $3,000. Proper business entity structuring costs somewhat more to establish and requires annual maintenance to hold up legally. The plan Robert did not have and the entity structure he did not maintain cost his family $80,000 and produced outcomes that $80,000 cannot reverse.

The families I work with who end up in situations like Carol’s are not the ones who did not care. They are the ones who intended to get around to it. Robert was that kind of man: organized, thoughtful, successful, protective of his family. He had mentioned the estate plan. He had thought about the business structure. Fifty-nine did not feel like an age that required urgency. A lawsuit he expected to win did not feel like a threat to Carol’s personal accounts.

The legal system does not weigh intention. It processes whatever is present when the court is opened.

The probate closed on day 847. Carol got the house. The lawsuit settled for less than the plaintiff had originally sought. The children received their distributions. The legal process produced, in the end, an outcome Robert probably would have chosen anyway.

But her youngest son had left college and not gone back. Her daughter had stopped coming home. Her oldest son carried a resentment that had nothing to do with Carol and nowhere else to go. And somewhere in the 847 days between Robert’s death and the closing of the estate, the family Robert spent his life building had become a different family than the one he left behind.

He did not intend for that to happen. He simply did not get around to preventing it.

The Estate Planning Blueprint Masterclass is a free one-hour class for families who want to build an estate plan that holds up. It walks through the three things every plan needs to keep probate out, protect children from avoidable conflict, and pass wealth to the next generation cleanly. Readers who recognized the patterns in this post and want to start building the structure that prevents them can register here:

Register for the Masterclass

Readers who would prefer to discuss a specific situation directly can book a free consultation here:

https://lastinglegacypro.com/estate-planning

Nathaniel Vale / The Legacy Blueprint