A man started a lending company because a predatory lender took his mother’s house.

He understood exactly what had happened to her. He had watched the process up close: the fine print, the rate adjustments, the fees she did not see coming, the timeline that compressed until there was no exit left. He knew the mechanics. And rather than simply resent the industry, he decided to build something different inside it.

On the first day he opened the doors, he wrote himself a letter.

It was not a mission statement for a wall or a framed values document for the lobby. It was a legal instrument. A preemptive surrender. The letter contained a signed power of attorney and a transfer of board authority, fully executable, to be activated under a single condition: if he ever abandoned the mission he was building the company to protect.

He gave the letter to the first employee he ever hired and said one thing: if he ever became what they were there to fight, use it.

Years passed. The company grew. And with growth came pressure: quarterly targets, investor expectations, competitive benchmarks. He did not change all at once. No one does. He started by allowing certain products he once would have refused. Then promoting them. Then, eventually, something that functioned as vulnerability targeting — identifying the customers most likely to accept unfavorable terms because those customers generated the highest margins.

The first employee opened the envelope.

A board meeting was called. Someone read the letter aloud — the one he had written on day one, in his own handwriting, when he still remembered exactly why he had started. He resigned the following week. Not because he was fired. Because he read what he had written and recognized he was no longer the person who wrote it.

This story is not about a corrupt man. It is about a structural reality that is far more difficult to argue with than corruption.

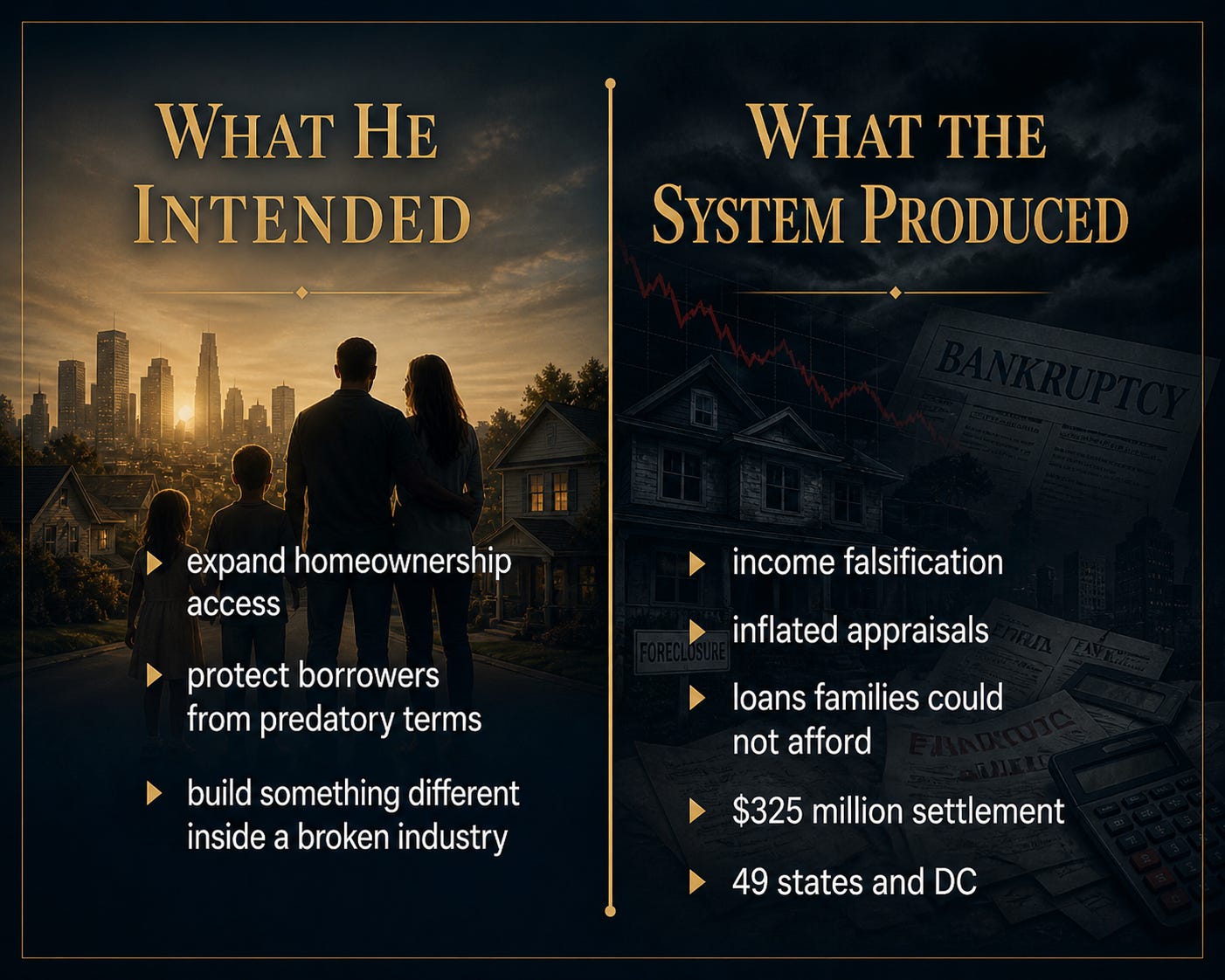

Roland Arnall survived the Holocaust as a child, co-founded the Simon Wiesenthal Center, and built Ameriquest Mortgage under the tagline “Proud Sponsor of the American Dream.” He genuinely believed he was expanding homeownership to people who deserved a chance. By the end, his employees were falsifying income documentation to put families into loans they could not afford — loans that would eventually take their homes. Forty-nine states and the District of Columbia filed against the company. Hundreds of thousands of borrowers were affected.

The pressures that had destroyed his mother’s financial life were embedded in the industry’s incentive design. The system did not require a villain. It produced the same behavior regardless of who occupied the chair.

The same pattern appears wherever systems have incentive structures that reward specific outcomes regardless of participant intent.

Henry Ford believed a company’s first obligation was to the people who built it. He wanted to pay his workers wages high enough to buy the cars they made. A court determined otherwise. Shareholders came first — not because Ford’s values were wrong, but because the legal structure of corporate obligation had already been defined. His personal conviction was irrelevant to it.

Dodge v. Ford Motor Co. was decided in 1919. The principle it established did not require anyone to be malicious. It required participation in a system whose design had already encoded the outcome.

Financial systems operate on the same logic.

A bank employee who recommends an overdraft protection product is not necessarily acting against a customer. They are operating inside an incentive structure that rewards the recommendation. A mortgage company whose loan officers approve applications at the edge of borrower capacity is not necessarily predatory in intent. The performance metrics, compensation structures, and competitive pressures of the industry point in that direction before any individual decision is made.

This is not a case for cynicism about financial institutions. Most of the people working inside them are not thinking about how to harm anyone. It is a case for structural awareness — for understanding that the outcomes a financial system produces are a function of how it was designed, not of the values of whoever happens to be operating it on a given day.

The families who get drawn into products that do not serve them are not primarily failing in discipline or judgment. They are operating inside systems specifically designed — through incentive structures, product architecture, and targeting models — to engage them at their most vulnerable moments.

Understanding that changes the frame.

The question is no longer whether the institution on the other side of the transaction means well. The institution’s intent is less predictable and less controllable than its design. The question is what the system is designed to do, who benefits when it expands, what behavior it rewards, and where the risk sits once the transaction is complete.

This pattern does not live in one corner of the financial system. It runs through all of them.

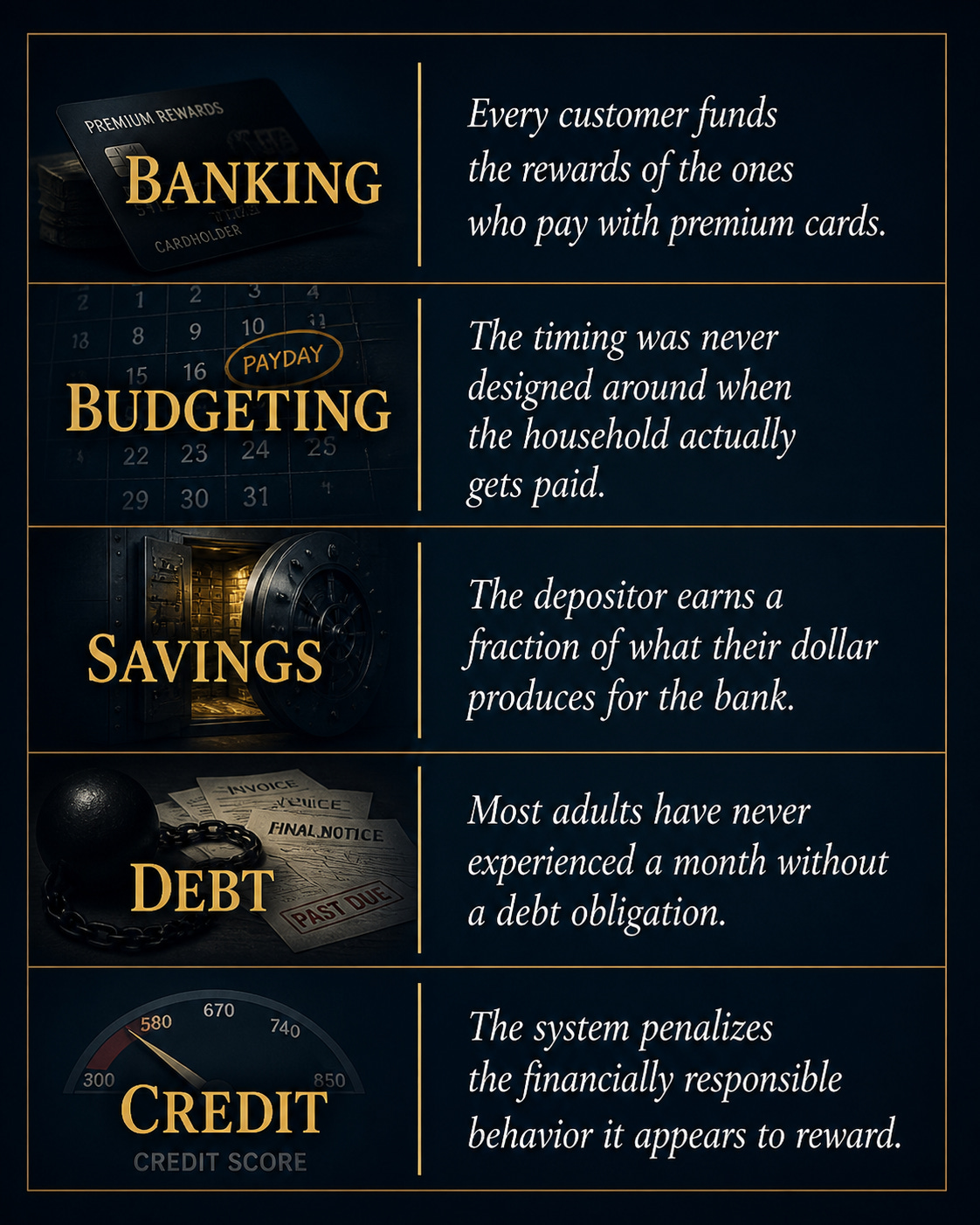

In banking, the interchange fees merchants pay on every card transaction are absorbed into the price of goods — meaning every customer, whether they pay with cash or card, is quietly subsidizing the rewards programs of premium cardholders without ever seeing a fee line on any statement. The merchant pays the fee. The merchant raises prices. Every customer pays a little more regardless of how they transact. The premium cardholder collects the points. Everyone else funds them.

In budgeting, the mismatch between when income arrives and when obligations fall due creates artificial shortfall periods that drive late fees and short-term borrowing — not because the household is underfunded but because the timing architecture was never designed around the household’s actual cash flow. The budget that looks balanced on paper fails in execution because payday and bill-due-date rarely align. That gap is not accidental. Payday lenders exist almost entirely because of it.

In savings, the same dollar a depositor earns 0.5 percent on is the dollar the bank lends at 7 to 25 percent depending on the product. The depositor’s money is the raw material the institution uses to generate its lending revenue. The depositor is compensated at a fraction of what that dollar produces. The household that feels responsible for maintaining a savings account in a traditional bank is the household subsidizing the bank’s lending margin without knowing it.

In debt, the normalization of lifelong borrowing is perhaps the most consequential design outcome in modern financial history. For most of recorded human history, debt was a condition of last resort — associated in legal systems across cultures with loss of autonomy, social standing, and in many cases personal freedom. The shift from that understanding to the present condition, in which a household carries debt from age eighteen to death without experiencing it as a crisis, was not organic. It was engineered through deliberate policy decisions, product sequencing, and cultural normalization across roughly seventy years. The system hands a young adult their first debt instrument before they have any framework for evaluating it, and then sequences the next obligation at every major life transition afterward. Student loan at eighteen. Car note at twenty-two. Credit cards throughout. Mortgage at thirty. By the time a household has the income and awareness to ask whether it wants to be in debt, it already is and has been for fifteen years. Most adults in the United States have never experienced a month without a debt obligation. The system did not produce that condition by accident.

In credit, closing a paid-off card damages the score. Paying off an installment loan can temporarily lower it. The household that eliminates debt and closes accounts — the behavior the system appears to reward — is penalized by the algorithm built to measure creditworthiness. That algorithm was designed by lenders to predict repayment behavior. Financial health and repayment prediction are not the same measurement. The credit score does not know the difference and was never built to care.

None of these require a conspiracy. They require a design. The design is working exactly as intended. The only variable is whether the household operating inside it understands what the design is optimizing for.

That is what this series is built to change.

The Design Literacy Series does not teach budgeting tips or debt payoff strategies or credit score hacks. There are thousands of places to find those. What it teaches is the layer underneath — the design logic of the systems those tips operate inside, the incentive structures that determine who benefits when each system expands, and the specific points where a household that understands the design makes a fundamentally different decision than one that does not.

Each post in this series takes one financial system and reconstructs it from the beginning. Not from a consumer’s perspective. From the designer’s perspective. What problem was this system built to solve. Who built it and when. Who benefits when it grows. What behavior does it reward. Where has it transferred risk onto the household without the household ever agreeing to assume it.

Banking. Budgeting. Savings. Debt. Credit.

Each one has a design. Each design has a history. Each history explains outcomes that most households have been attributing to their own decisions for years.

The man in the opening of this piece wrote himself a letter on the first day because he understood something most people only learn after the damage is done: that the system he was entering had its own logic, its own incentives, and its own direction of pull. He thought awareness would be enough to resist it. It was not. But his story is not an argument for helplessness. It is an argument for preparation.

The households that navigate financial systems most effectively are not the ones with the highest incomes or the most discipline. They are the ones who understood the terrain before they entered it. Who asked the right questions before the decisions were made. Who stopped treating institutional approval as advice and started treating it as one party’s answer to one party’s question.

That is the literacy this series builds.

The next post begins with the system most households interact with before they understand any of the others — and the one whose design is most deliberately invisible to the people inside it.

Subscribe to follow the series. Every post will be here when it lands.

If this series is raising questions about how your own financial systems are structured, including what happens to what you have built when you are no longer here to manage it, that question has its own system and its own design. The free webinar at Lasting Legacy Pro covers it in the same plain-language, structure-first approach this series uses.

Register for the free webinar: https://lastinglegacypro.com/webinar

Ready to talk through your specific situation: https://lastinglegacypro.com/consultation