The 100-Year Plan Post 06

a Legacy Blueprint series on how ordinary families build Quiet Money. One overlooked account, one written instruction, one principal that is never touched, compounding quietly for a hundred years. Each post in the series shows the plan applied to a different family, a different vehicle, a different overlooked seed.

The conversation happened at the diner across from the precinct, on a Tuesday in March.

He had been stopping at Marlene’s for coffee on his way to shift for six years, ever since he transferred to the detective bureau. The same booth most mornings if he had time, the counter if he was running late. He knew Walter from the counter.

Walter was somewhere in his late seventies. The kind of man who had worked with his hands at some point in his life and clearly was not working anymore. He wore the same plaid shirt three days a week. They had built the kind of friendship that lived inside small talk over six years of crossing paths most mornings. The weather. The score from the night before. The detective’s son, born the previous year, whose photograph Walter had asked to see on three separate occasions.

The detective had been thinking, on and off for two weeks, about something he could not quite name. His father had retired the year before. The pension was sufficient, the house was paid off, the life was honorable. He had been raised in that life and he had no quarrel with it. But there was a question that had started running underneath everything he did, and he had not figured out how to phrase it, even to his wife.

The question had to do with what came after his own father, after himself, after a son who was now one year old. The question was not about money exactly. It was about whether there was anything his family had ever built that would still be there in a hundred years. His grandfather had retired from the force in 1989 with a pension and a house. His father had retired the previous year with the same. He was thirty years old, six years into his own career, and he could see the same arc ahead of him. Three generations of honest work, three pensions, three paid-off houses, no mechanism that compounded across the family line.

On Tuesday in March, on his way out, Walter asked him if everything was alright.

The detective sat down on the stool next to him. He said the thing he had not yet been able to say to his wife. It took him about three sentences. His grandfather had been a cop, his father had been a cop, he was a cop, and not one of them had built anything that compounded across the family line. He was thirty years old and he could already see the same trajectory ahead of him, and he did not know how to feel about it.

Walter listened to all of it without interrupting. When the detective finished, Walter set his coffee down.

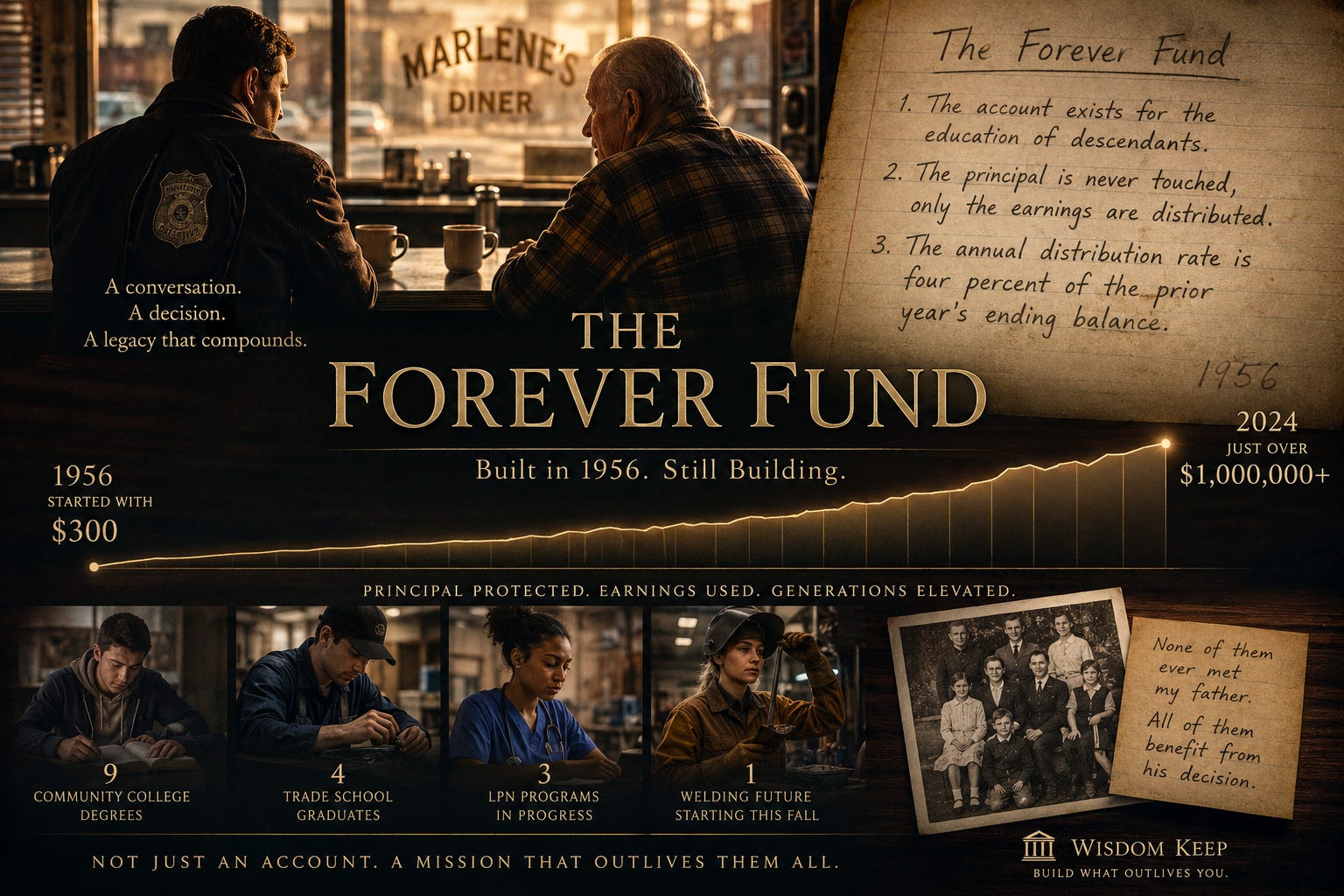

“My father did something about this in 1956,” he said.

Walter’s father had been a millwright at a paper plant in Pennsylvania. He had finished the eighth grade. He had three sons, of which Walter was the youngest. In 1956 he had opened a brokerage account at a regional bank with $300 he had saved, and he had arranged for a monthly contribution of $15 to come out of his paycheck automatically.

The instructions he wrote, signed, and put in the account folder were three sentences long.

The account exists for the education of descendants. The principal is never touched, only the earnings are distributed. The annual distribution rate is four percent of the prior year’s ending balance.

He had given the account a name. He had written it across the top of the page in pencil.

“The Forever Fund,” Walter said. “That’s what he called it.”

He drank a swallow of his coffee.

“My oldest brother managed it after my father passed. Then me. I have been the steward of it for thirty-one years now. We added to it whenever we could. My brothers contributed when they were earning. I have been adding for three decades myself. Birthday checks. Tax refunds. The two thousand my father left specifically marked for the account when he passed. The principal has never been touched. The contributions are what added up alongside the compounding.”

The detective asked him how much was in it.

“Just over a million now,” Walter said. “It has funded community college for nine of my father’s descendants. Trade school for four. Three of my grandnieces are in licensed practical nursing programs right now. A great-granddaughter is using it for welding tools this fall. None of them ever met my father. None of them know his first name. They all know the account exists. They all know what it is for.”

The detective stayed on the stool for another forty minutes.

He opened his own account the following Saturday.

The structure was the one Walter had described, scaled to his own circumstances. A brokerage account in his son’s name, custodial until majority, then transferred to a simple trust he would draft with a Legal Document Preparer the following year. The opening deposit was $1,000. He set up an automatic monthly contribution of $100, scheduled for the day after his paycheck cleared.

The investment instruction matched Walter’s father’s logic, updated for the current era. A U.S. Treasury bond ladder. Bonds maturing in two, four, six, eight, and ten years, rotating as each rung matured. The same instrument the most conservative portion of every university endowment leans on for long-horizon stability. Not because it is exciting. Because it is boring, and boring is what an endowment needs.

He wrote a single page of instructions and put it with the account paperwork. At the top of the page, in his own handwriting, he wrote the name.

The Forever Fund.

Below the name, three rules.

The account exists for the education of descendants. Education is defined broadly: tuition at any accredited institution, trade school costs, certification programs, community college, apprenticeship tools, books required for any of the above.

The principal is never touched. Only the earnings are distributed.

The annual distribution rate is four percent of the prior year’s ending balance, paid out on September first of each year to one qualifying descendant. If no descendant qualifies in a given year, the distribution stays in the account and compounds.

That was it. One page. He signed it, dated it, and put it in the file with the brokerage statements.

The math, walked slowly, looks like this.

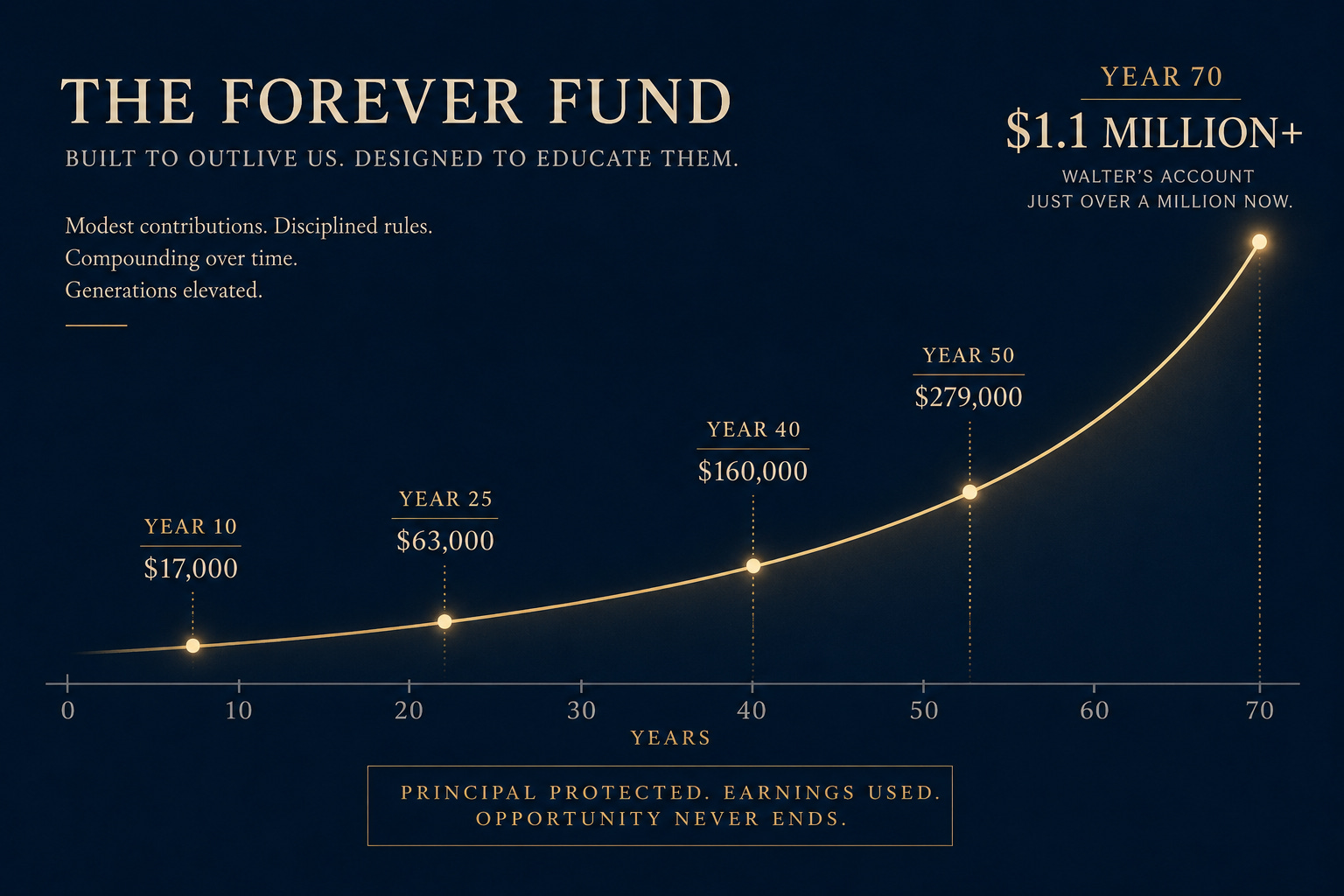

A Treasury bond ladder over long horizons has produced average annual returns in the range of four to six percent. The number varies by era and by the specific maturities held. Using five percent as a working assumption, the Forever Fund develops the following way.

At the end of year ten, the account holds approximately $17,000. The annual distribution at four percent would be $680. He is forty. His son is ten. There is no one yet to receive a distribution, so the four percent stays in the account and compounds.

At the end of year twenty-five, the account holds approximately $63,000. The annual distribution at four percent would be $2,500. He is fifty-five. His son is twenty-five and is one year into the police academy himself, the fourth generation in uniform. The academy is paid for. The son does not draw. The distribution stays in the account.

At the end of year forty, the account holds approximately $160,000. The annual distribution at four percent would be $6,400. He is seventy. His son is forty, a sergeant. His first grandchild is eight years old, ten years away from any qualifying use. The compounding continues.

At the end of year fifty, the account holds approximately $279,000. The annual distribution at four percent is $11,160. He is eighty. His son is fifty. His grandchildren are between fifteen and twenty-three. The first qualifying use arrives. A granddaughter enrolls in a welding certification program. The account distributes $4,800 for tuition and tools. The remaining $6,360 of that year’s earnings stays in the account.

The principal is untouched. The next year, the account starts from a slightly higher base, and the cycle repeats.

What $11,000 a year actually buys is the part most family conversations skip over.

The reflex is to picture a four-year university. That is one path. It is not most of the paths the Forever Fund will actually fund across a hundred years of operation. A four-year degree at a public in-state university is one option, partially covered. A welding certification at a community college is another, fully covered. A licensed practical nursing program. Books and lab fees during an apprenticeship. A coding bootcamp. A commercial driver’s license course. Tools required to start an electrical apprenticeship. The down payment on a uniform and academy fees for a great-grandson who decides he wants to wear the badge too.

The instruction the detective wrote was deliberately broad. He had grown up around the families of officers in his father’s precinct. He knew that children of police officers often went into the trades or service careers rather than four-year degrees, and he knew the financial strain of paying for those credentials out of pocket. He did not want any descendant of his to face that strain. The account would cover the path the descendant chose, not the path the family preferred.

This matters because the structural assumption that generational education wealth equals university tuition is wrong in ways that close off most of the actual uses. A family endowment that funds only four-year degrees will be drawn from rarely. A family endowment that funds every legitimate form of credentialed learning, including the credential a granddaughter would pay for to enter nursing and the credential a great-grandchild would pay for to enter law enforcement, will be drawn from often.

There is something the detective understood after his conversation with Walter that most founders of new endowments have to take on faith.

He had seen one running.

Walter’s account was a working version of what the detective was about to start. Seventy years of compounding. The original $300 still in there, sitting inside a balance that had crossed a million. Nine descendants put through community college. Four through trade school. Grandnieces in nursing programs and great-grandchildren in welding certifications. The account was not theoretical. It was a fact in the world, sitting in a regional bank in Pennsylvania, opened in 1956 by a millwright who had finished the eighth grade.

This is the piece most people who try to start an endowment from scratch never get. They are asked to trust the math without ever having seen the math operate. They are asked to plant something whose mature form arrives long after they are gone, on faith in a structure they have only read about. Most people cannot do that, and the failure is not a failure of character. It is a failure of introduction.

What Walter gave the detective at the diner counter that Tuesday in March was not money. It was the introduction. He had shown the younger man what the destination looked like, in a specific bank, in a specific family, with a specific seventy-year history. The detective walked out of the diner not believing the math abstractly but knowing what the math becomes.

The Forever Fund is in the public domain. The mechanism has been available to ordinary families for centuries, and it does not care what the founder does for a living. A millwright built the version Walter showed the detective. A police officer is building the version that comes next. The same structure runs quietly in the families of teachers, soldiers, nurses, accountants, mechanics, and shop owners, in accounts no one outside the family knows about. The compounding is indifferent to occupation. What it responds to is the rule and the timeline.

What is rarely in the public domain is the introduction, the person willing to sit on a stool next to a younger person and say, my father did something about this in 1956, and here is what it became.

A police officer at thirty with $1,000 and an auto deposit can build the same instrument Walter’s father built. The numbers start smaller. The mechanism is identical. The compounding does not know what the founder does for a living, and it does not require the founder to figure the structure out alone.

What it requires is the rule. The principal is not spent. Everything else, including the eventual million-plus balance and the great-great-grandchildren who will draw from it, is just the rule running on autopilot across a long enough timeline to do its quiet work.

The detective never thanked Walter for the conversation. He did not have to. Walter knew, the way old men sometimes know things, that the conversation had landed exactly where it was supposed to land. The detective stops at Marlene’s most mornings still. He sits on the same stool. He has shown the photograph of his son to Walter four more times since that Tuesday in March. He has not yet shown Walter the page with The Forever Fund written across the top, but he keeps it folded in his wallet, and he plans to, the next morning he has the time.

If something has been sitting in an account without a purpose, or if the structure described here matches something already half-built in a family, the Estate Planning Blueprint Masterclass walks through how to formalize it. The principles are the same whether the seed is $1,000 or $100,000. The mechanism scales down as well as it scales up. And the introduction is the part most families never get on their own.

The Estate Planning Blueprint Masterclass is a free one-hour class for families who want to build an estate plan that holds up. It walks through the three things every plan needs to keep probate out, protect children from avoidable conflict, and pass wealth to the next generation cleanly. Readers who recognized the patterns in this post and want to start building the structure that prevents them can register here:

Register for the Masterclass

Readers who would prefer to discuss a specific situation directly can book a free consultation here: