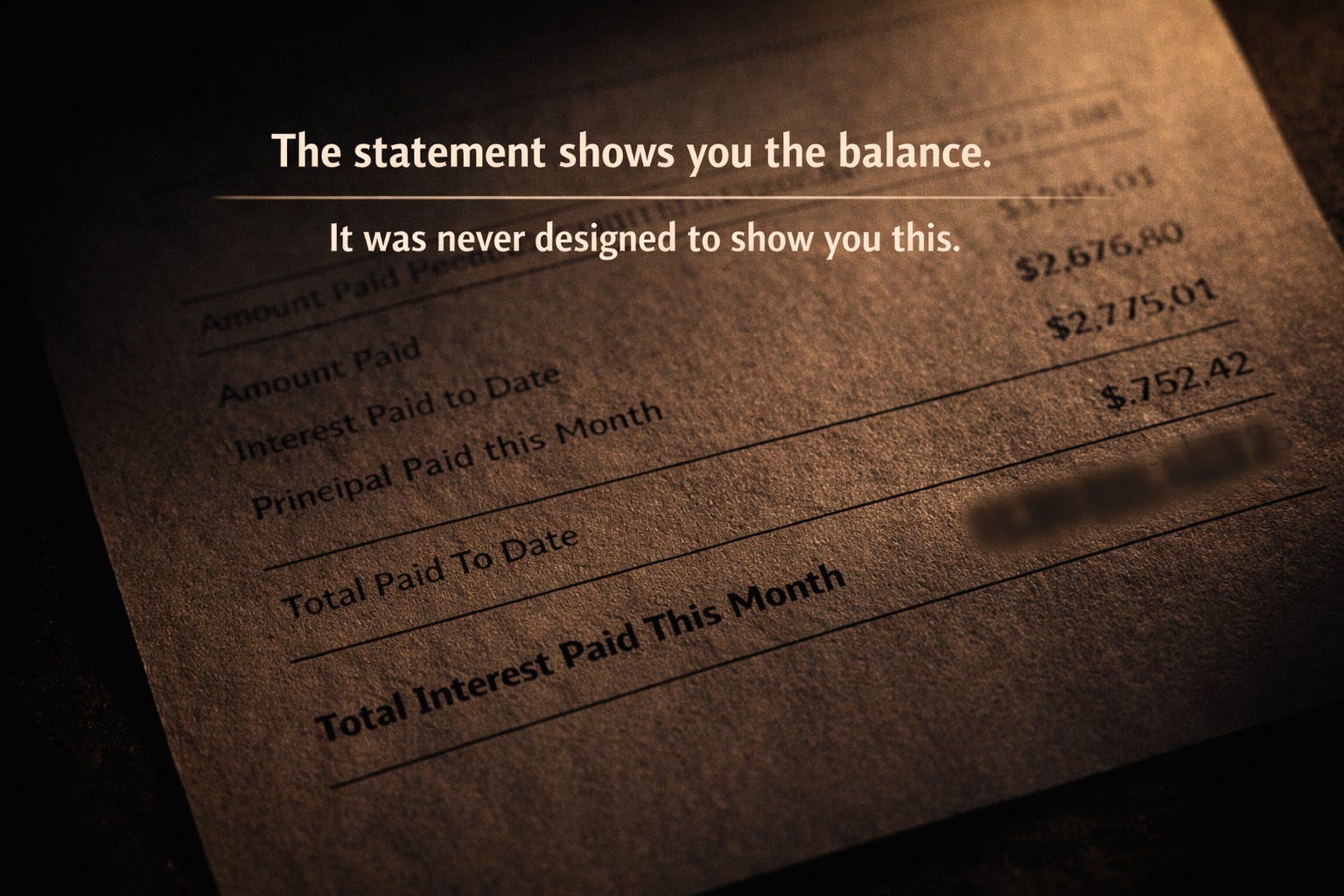

The balance on your credit card statement is not what you owe. It is what you owe so far.

The actual cost of carrying that balance — the full transaction price, start to finish — is a number your statement was not designed to show you. Most people who have been in credit card debt for years have never seen it. Not because it’s hidden in fine print, but because nobody added it up and put it somewhere visible. The system has no structural reason to do that for you. You have every reason to do it for yourself.

This is not about how you got here. It is about what here is actually costing you — because most people tracking the balance are tracking the wrong number entirely.

The Real Price Is Not the Balance

Take a $10,000 credit card balance at 29 percent interest. Over the life of that debt, paying minimums, you will surrender somewhere between $18,000 and $22,000 in interest alone. That’s the number most people stop at when they think about the cost of debt. It’s a significant number. It’s also the smaller of the two losses.

The larger loss never appears on a statement.

That $250 monthly minimum payment — redirected instead into an account compounding at a modest 7 percent annual return — becomes approximately $79,000 over the same payoff period. Hold it for 30 years and it crosses $300,000. The money you are sending to service that balance is not just paying for past purchases. It is permanently vacating a future. Not a theoretical future. A calculable one.

That is what the debt costs. Not $30,000. Potentially hundreds of thousands of dollars in compounding that will never happen because the capital was extracted, monthly, in increments small enough to feel routine.

The system is designed for those increments to feel routine. That design is not accidental.

You Are Not Being Punished. You Are Being Grouped.

Here is the piece that almost nobody knows, and it changes how the entire structure looks.

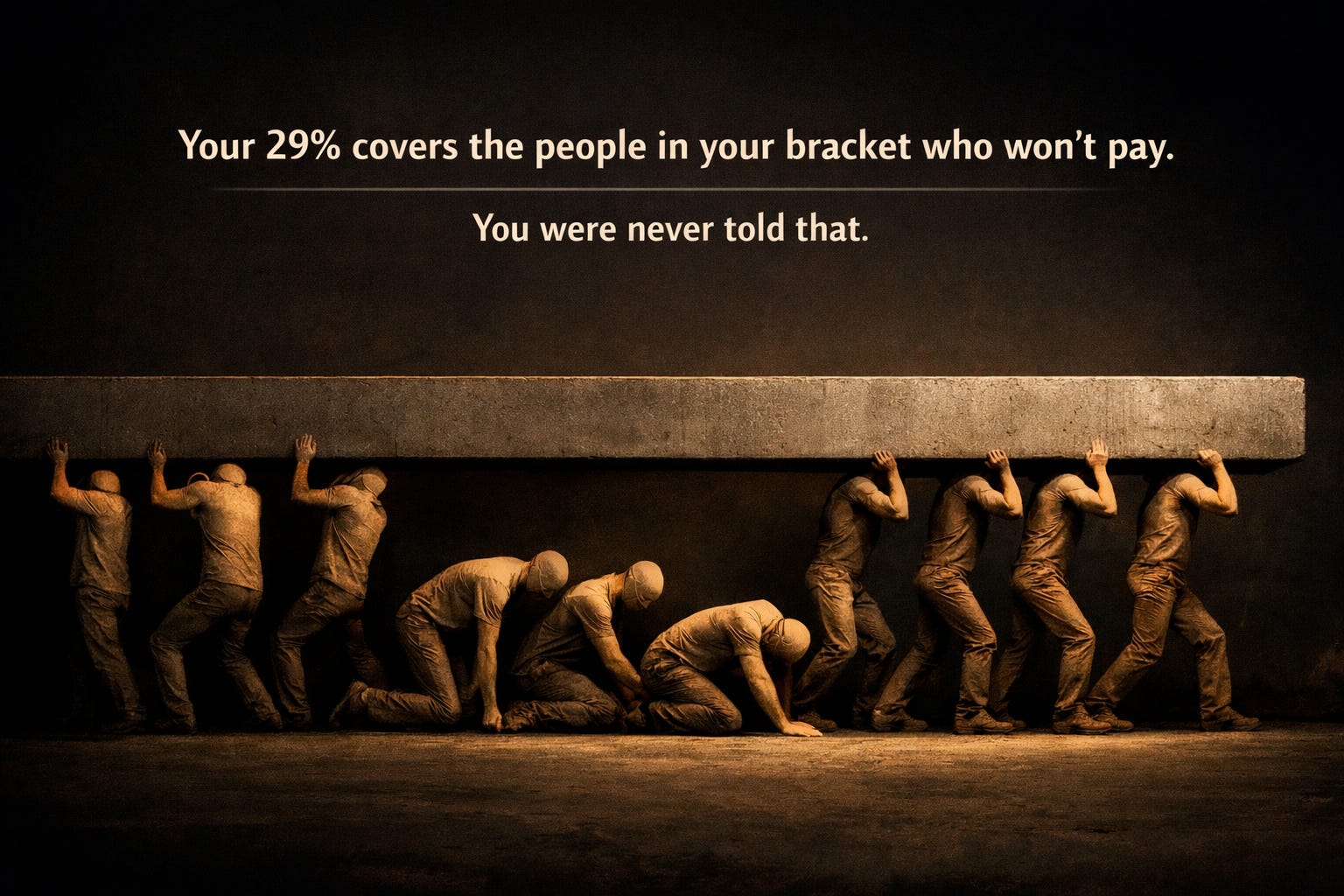

When a credit card issuer assigns you a 29 percent interest rate, they are not punishing you for your credit score. They are pricing you for the group your credit score places you in. This is actuarial logic — the same math that underlies insurance premiums — and it operates the same way.

The issuer knows, with considerable precision, that within your risk bracket a certain percentage of cardholders will default. Those defaults represent real losses. The interest rate charged to everyone else in the bracket is calibrated to cover those losses and generate the target return on top. The customers who pay — including the responsible ones who just hit a rough patch and ended up with a lower score — are collectively funding the losses from the ones who won’t.

You are not being charged 29 percent because of what you did. You are being charged 29 percent because of the statistical behavior of the group you were sorted into. Your individual payment history, your individual circumstances, your individual intentions — none of that is the variable. The variable is the actuarial model for your bracket.

This matters because it reframes the relationship entirely. You are not in a conversation with an institution that assessed your character. You are inside a pricing structure designed around group behavior. Understanding that is the first step toward navigating it rather than internalizing it.

The Institution Does Not Want You to Default

This is the part that feels counterintuitive at first.

The credit card issuer does not want you to miss payments. It does not want you to default. Default is a loss — a debt sold to collections at a fraction of face value, a customer relationship that ends, revenue that stops. Default is the outcome the model accounts for as a cost of doing business, not the outcome it optimizes for.

The outcome it optimizes for is you, paying minimums, indefinitely.

A cardholder making minimum payments on a $10,000 balance at 29 percent is, from the institution’s perspective, a near-perfect customer. The balance barely moves. The interest charges continue. The account stays current. There is no default risk because the customer is paying. There is no payoff risk because the minimum is designed to extend the balance as long as mathematically possible. The account generates consistent, predictable revenue for years — sometimes decades.

The minimum payment is not a concession. It is the mechanism. It exists to keep the guaranteed win running.

And the institution already knows your final number — how long you’ll carry the balance, how much you’ll pay in total, what your account is worth to them over its lifetime. They modeled it before they approved you. You, in almost every case, have never calculated it at all.

That is the asymmetry. Not malice. Just two parties operating inside the same system with radically different amounts of information about how it ends.

Make the Invisible Number Visible

There is one practical thing that cuts through this more effectively than any budgeting tactic, any payoff strategy, any motivational framework.

At the end of every budget session, write down how much you paid in interest that month across every debt you hold. Every credit card. Every loan. Every balance. Add them up into a single number and put it at the bottom of the page.

Not the payment. The interest portion of the payment — the amount that reduced your balance by zero dollars.

Most people have never done this. The interest charge is buried inside the minimum payment, spread across multiple accounts, never surfaced as a single figure. When it stays invisible, it fades into the background as a vague, uncomfortable awareness that debt is expensive. When you write down the number, something shifts.

You may find that you made $1,300 in payments last month and $1,100 of it was interest. That you worked, earned, allocated — and $1,100 of it went to servicing the cost of carrying balances rather than building anything. That number, seen clearly, does something that no amount of advice about the importance of paying down debt ever quite accomplishes. It makes the extraction visible. And once it’s visible, it stops being abstract.

This is not a trick. It is just accounting — the kind the statement doesn’t do for you, because the statement was not designed with your clarity in mind.

There Is No Shortcut to the Other Side

It is worth being direct about something, because a lot of financial content isn’t.

There is no mechanism that makes getting out of credit card debt fast or painless. The math is the math. You spend less than you earn, you direct the difference toward the highest-rate balance first, you hold that discipline for however long it takes, and eventually the balance is gone. The people searching for the smarter method — the trick, the arbitrage, the thing someone else figured out — are often the same people who ended up in the deeper hole. The search for the shortcut is part of the pattern the industry understands and designs around.

What you can control is the information you’re working with and the systems you put in place to act on it. You can know what the debt is actually costing. You can know why the rate is what it is. You can make the monthly interest extraction visible instead of letting it fade. You can treat the minimum payment as a floor you never touch rather than a target you hit.

None of that changes the math overnight. But operating the system with an accurate understanding of how it works is a different position than operating it blind.

The first position still has a long road. The second one doesn’t necessarily end at the same place.

This essay is part of the Wisdom Keep series: The Price of Not Knowing. Companion video this week: “The Sovereign Allocation Model vs. The Reactive Obligation Budget”