The Average Wedding Costs $30,000. This Family Pays for It Without Going Into Debt. Every Time.

A family tradition that starts every marriage debt-free.

Before we dive in: I'm hosting a free masterclass on exactly this strategy. How to turn existing accounts and overlooked assets into permanent family structures that keep giving long after you are gone. If you have something sitting unused and want to know what it could become, this is for you.

→ Register for the Estate Planning Blueprint Masterclass

https://lastinglegacypro.com/webinar

Her granddaughter had not said the number out loud yet.

She had been engaged for three weeks. She was happy, genuinely, visibly happy, but something was running underneath it. Her grandmother could see it in the way she kept opening her phone and setting it back down. The way she changed the subject when the wedding came up at dinner.

Finally, at the kitchen table over coffee, it came out.

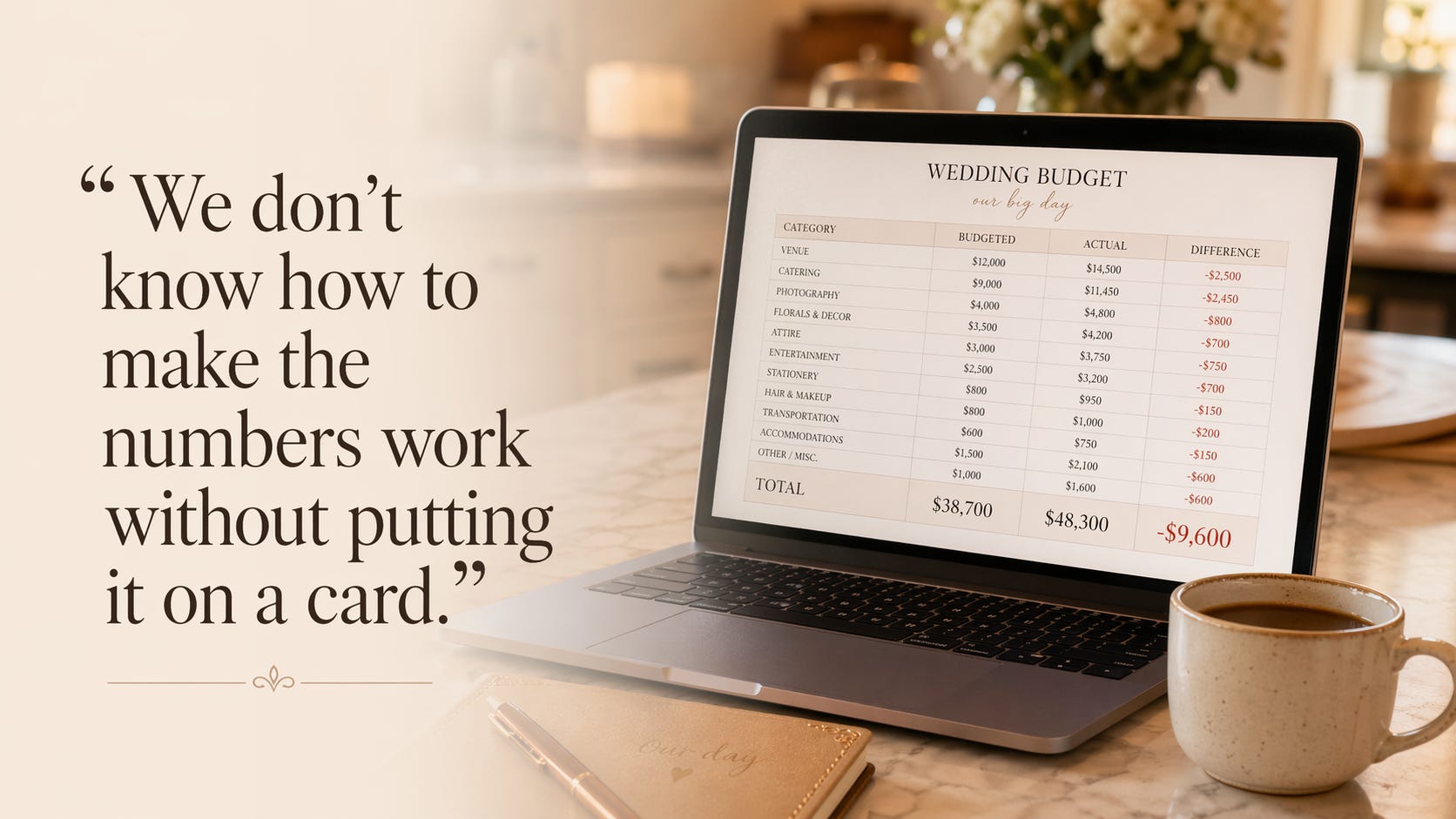

“We looked at venues last weekend. The one we both loved is $8,500 just for the space. That’s before food, before the photographer, before anything else. We’ve been saving but not for this. We don’t know how to make the numbers work without putting it on a card.”

Her grandmother sat with that for a moment.

She had been married herself for forty-one years before she was widowed. She remembered the weight of the early years: not the love, which was never in question, but the money. The argument in month three about a credit card balance neither of them had expected to still be carrying. The way that balance, $3,200 when they got home from the honeymoon, had taken eleven months to pay off. The way financial stress has a specific texture in a new marriage, a particular kind of friction that wears on things quietly and is not always named for what it is.

She did not want that for her granddaughter. She did not want it for any of them: the ones getting married now, the ones not yet born who would someday sit at a kitchen table with a number they could not say out loud.

She is not alone in that feeling. Fathers have sat across from me in that same chair, describing the same thing from a different angle. A father who spent three years quietly saving to contribute to his daughter’s wedding, handed over what he had saved, and watched it disappear into a single Saturday. He was glad to give it. He also knew that the next daughter would require the same process to start over, and the daughter after that, and someday the granddaughters. Generous, repeated, and always temporary.

When she came to see me, she had a clear-eyed question.

“Is there a way to make sure this never happens again in our family?”

There is.

What she was asking about has a name most families have never heard applied to themselves. An endowment.

Universities use them to fund scholarships in perpetuity. Hospitals use them to fund research wings that carry a donor’s name for a hundred years. The mechanism is straightforward: a sum of money is placed into an investment account, only the growth is ever spent, and the principal compounds forever. The gift never runs out because the source never gets touched. It is one of the oldest wealth-preservation structures in existence, and for most of history it has been the exclusive territory of institutions and families with generational fortunes.

A grandmother with a $40,000 account she no longer needs can build the same thing.

The seed does not have to be large. The mechanism works the same way at $40,000 as it does at $40 million. What it requires is not a large sum but a clear instruction: use only the growth, never the principal, and define exactly what the growth is for. Most families have never done this not because they lacked the resources but because nobody ever told them it was available to them.

Most families who want to help with a wedding do it the traditional way. They save over several years, contribute what they have accumulated, and the money is gone the day the celebration ends. The next child who gets married starts the same process over. The parents save again, contribute again, and the cycle resets with every generation.

A wedding endowment does something structurally different. Instead of saving to spend, the family saves to seed. The contribution happens once. The principal never leaves. Every wedding that follows draws from the growth that principal produces, not from a savings account that has to be rebuilt each time. The family sets this up once and funds every wedding forever.

The difference is not the amount. A family that saves $40,000 and spends it on one wedding has done something generous. A family that seeds $40,000 into a trust has done something permanent.

Here is the structure.

A fixed trust contribution is available to every member of the family for their first wedding. Not to cover the full event: the trust is not writing a blank check for the venue of anyone’s dreams. It is providing a meaningful contribution toward the celebration, enough to keep the couple from starting their marriage carrying debt for the party.

The amount is set in the trust document and applies equally to every family wedding, every generation, without negotiation and without anyone having to ask. It is simply what this family does.

That consistency matters more than the dollar amount. A family where every child knows, from the time they are old enough to understand, that there is something set aside for their wedding day carries a different relationship to that milestone. The planning starts from a different place. The stress has a different shape.

The founder of the trust sets the contribution amount in the trust document itself. Once it is written, it applies to every family member equally across every generation. There is no deciding on a case-by-case basis, no comparing what one sibling received versus another, no uncomfortable conversations about fairness. The document makes the decision, and the decision was made with love and clarity before anyone was even engaged.

The numbers behind a wedding endowment tell a story most people have not seen before. They start with how much the alternative actually costs.

Couples who finance part of their wedding carry an average of $11,000 to $13,000 in wedding-related debt after the celebration. At a typical credit card rate, a couple making consistent payments on $12,000 will spend the first two years of their marriage still paying for the reception. The flowers are a memory. The debt is still a line item on the monthly statement.

That debt does not sit quietly. Research on couples and financial stress consistently shows that money arguments are among the leading predictors of marital difficulty in the early years, and debt carried into a marriage from the start adds a specific weight to those early conversations. The couple is not arguing about the future. They are still settling the cost of the past.

The endowment removes that weight before the marriage begins.

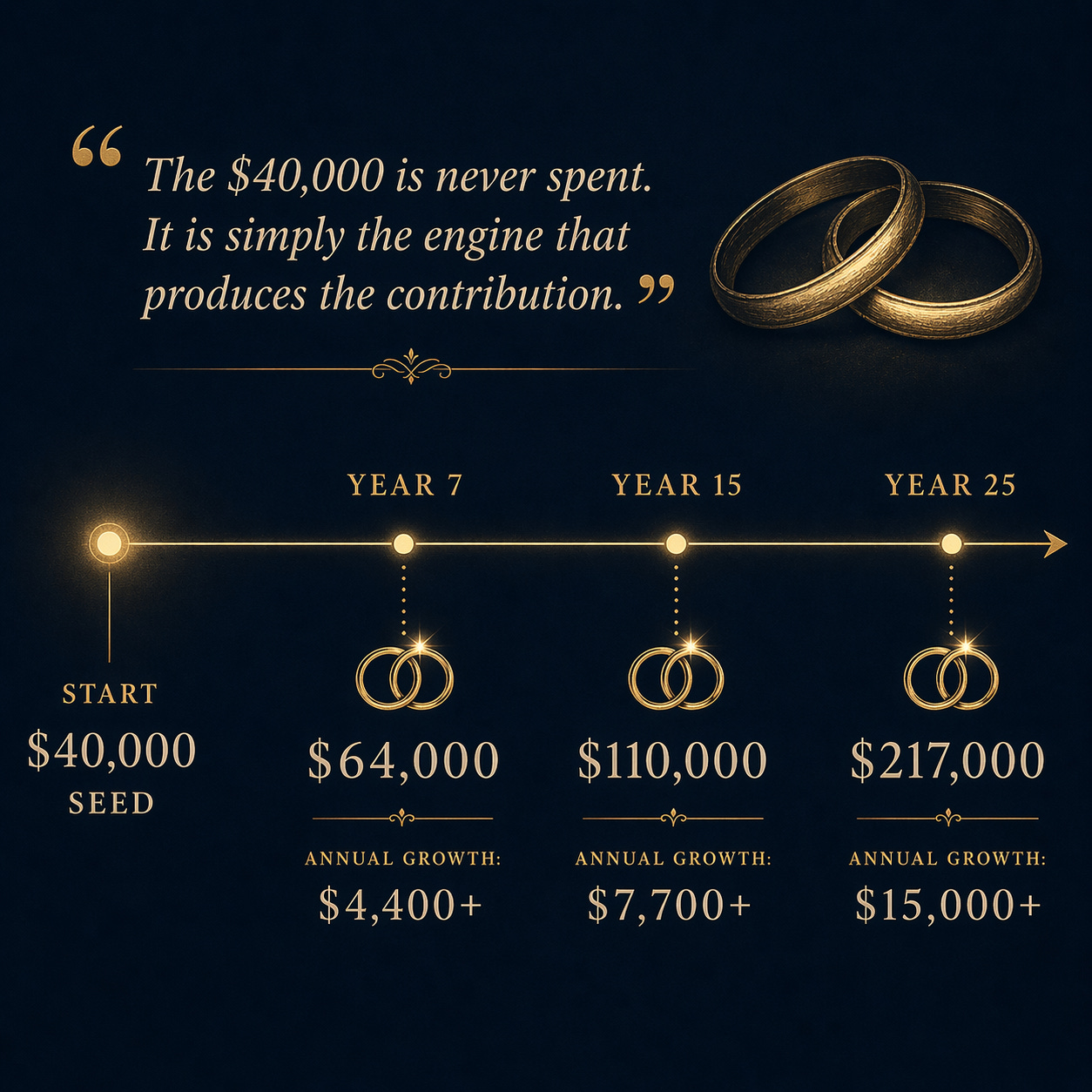

A $40,000 seed at 7 percent annual growth:

In year one, the account earns roughly $2,800. The trust is not ready to fund a wedding contribution yet. It is still growing.

By year seven, the account has grown to $64,000. Annual growth exceeds $4,400. A meaningful contribution ($5,000 to $8,000) is available from accumulated growth, with the principal still intact.

By year fifteen, the principal sits at $110,000. Annual growth exceeds $7,700. The trust can make a substantial contribution to one wedding per year indefinitely, every dollar coming from growth, the base never touched.

By year twenty-five, the account has reached $217,000. Annual growth exceeds $15,000. In a year with no wedding, that growth stays in the account and compounds. In a year with two weddings, the trust draws from accumulated growth across prior years and funds both.

The $40,000 is never spent. It is simply the engine that produces the contribution, generation after generation, for as long as the family exists.

What happens when no one gets married for ten years?

Nothing bad. The trust waits, and while it waits, it compounds. The decade with no draws produces the most growth the endowment will have ever seen. Whatever wedding follows that quiet decade receives a contribution from a fund that has been building without interruption for ten years. The gift is larger than it would have been. The family that waited benefits from the wait.

What happens when two siblings get married in the same year?

The trust accounts for it. In years with multiple draws, the trustee pulls from accumulated growth across prior quiet years. The math works because the endowment is designed to run across generations, not calendar years. A single-year spike does not destabilize a fund that thinks in decades.

Some families set the contribution as a fixed dollar amount: $10,000 per wedding, regardless of the total cost. Others set it as a proportional match, where the trust contributes up to a certain percentage of documented wedding expenses. Either approach keeps the structure clear and removes the negotiation that can complicate family money.

One clause many families include: the contribution applies to a first marriage only. This is not a restriction so much as a recognition. The beginning of a life together is the moment worth protecting. The trust is a one-time foundation per person, a single act of setting someone up well before the life they are building actually starts.

This is the kind of thinking The Legacy Blueprint is built around — simple structures that protect the people you love from the weight you know from experience. Subscribe free and get every post delivered to your inbox.

The gift is not the money.

Anyone who has been married understands this intuitively, even if they cannot immediately articulate it. The wedding itself passes in a day. The photographs age. The flowers are gone before the week is out. What remains is the marriage, and the conditions under which it begins.

A couple that starts their marriage carrying debt for a celebration they could not quite afford is not starting from zero. They are starting from behind. The first year of a marriage is demanding under the best conditions: two people building a shared life, negotiating habits and finances and expectations they did not fully know they had. Adding the weight of a debt incurred for a single day makes that first year harder in a specific, preventable way.

The grandmother who sat across from me was not trying to buy her granddaughter a perfect wedding. She understood perfectly well that no trust contribution guarantees a good marriage. What she wanted was to remove one source of early pressure, to give the couple a foundation that was clean, that did not have debt built into its first chapter.

That is what the trust does. Not extravagance. Not excess. A clean start.

Picture the moment the tradition activates for the first time.

A granddaughter calls her father to say she is engaged. He congratulates her, asks about the proposal, listens to every detail. Then, before she can say anything about venues or budgets or how they are going to make the numbers work, he says something she did not expect.

“There is something your grandmother set up for this. You don’t have to worry about the money the way we did.”

That conversation does not happen in most families. It happens in families that built something for it.

She planted that seed: $40,000, structured carefully, set in motion for every wedding that will ever happen in her family line. For a great-granddaughter she will never meet, who will someday sit at a kitchen table and not have to carry the number alone.

Every family has its own version of that kitchen table conversation: the number that is hard to say out loud, the stress that runs underneath a happy occasion. A wedding endowment does not eliminate the conversation. It changes what the conversation is about. Instead of “how do we pay for this without going into debt,” it becomes “here is what the family has set aside for you, now let’s talk about what you want your day to look like.”

That is a different conversation. It produces a different beginning.

That is what legacy looks like when it is built on purpose.

If you have watched someone you love stress about wedding costs, or if you have been the parent quietly saving and spending and starting over, this kind of structure may be worth understanding. The Estate Planning Blueprint Masterclass walks through how to build an endowment like this from what you already have, without complexity and without a large estate as a starting point.

→ Register for the Free Estate Planning Blueprint Masterclass

https://lastinglegacypro.com/webinar

If you are ready to talk through what this looks like for your family specifically:

→ Schedule Your Free Consultation

https://lastinglegacypro.com/consultation

The kitchen table conversation is going to happen in your family one day. The only question is what kind of conversation it will be.

— Daniel Lasting Legacy Pro

Thanks for reading The Legacy Blueprint. If this resonated with you or someone in your family is planning a wedding, subscribe free — a new piece like this lands in your inbox every week.