He Never Got to Try. His Grandchildren Will.

How one trust becomes a permanent family venture fund for every entrepreneur in the line.

Before we dive in: I’m hosting a free masterclass on exactly this strategy. How to turn existing accounts and overlooked assets into permanent family structures that fund the next generation long after you are gone. If you want to know what you could build with what you already have, this is for you.

—> Register for the Estate Planning Blueprint Masterclass

https://lastinglegacypro.com/webinar

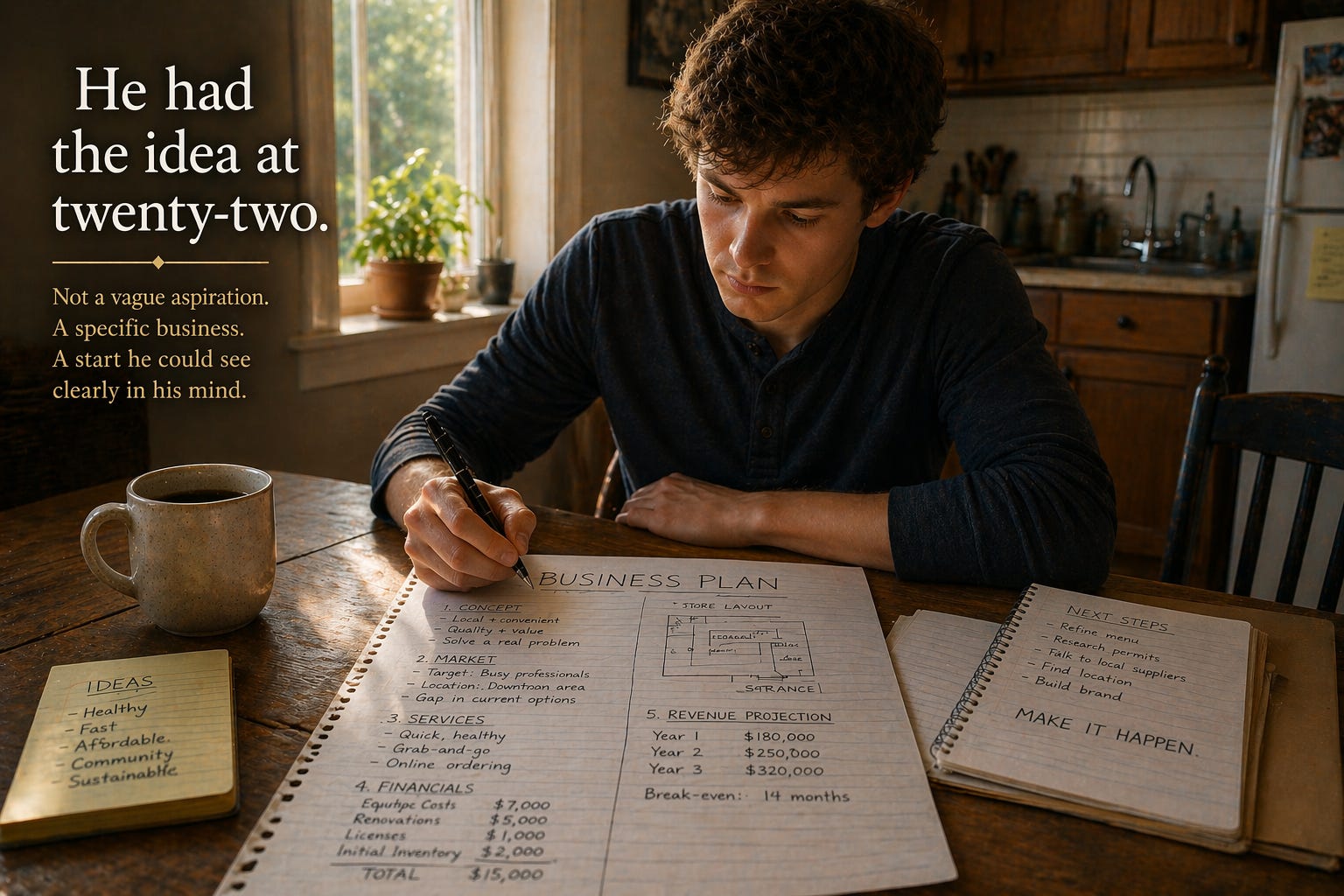

He had the idea at twenty-two.

Not a vague aspiration. A specific business. He had identified a gap in his local market, sketched out the model on notebook paper, and run the numbers more times than he could count. The numbers worked. The idea was sound. He talked to people who knew the industry and none of them told him it was wrong.

What he did not have was $15,000.

Not for lack of trying. He had saved what he could working construction. He had asked two banks and been told he did not have enough credit history. He had looked into small business loans and found that the application process assumed a level of collateral he did not have at twenty-two. The people around him did not have the capital either. His family was working class, careful with money, genuinely supportive, and completely unable to help him get started.

The business did not happen. He went back to construction, built a good life, raised a family he was proud of. But the idea stayed with him the way unmade things tend to stay. Not as regret exactly. As a question he never stopped turning over.

What would have happened if the money had been there?

He never found out. The window closed, the business stayed unbuilt, and forty-five years passed before he sat across from me.

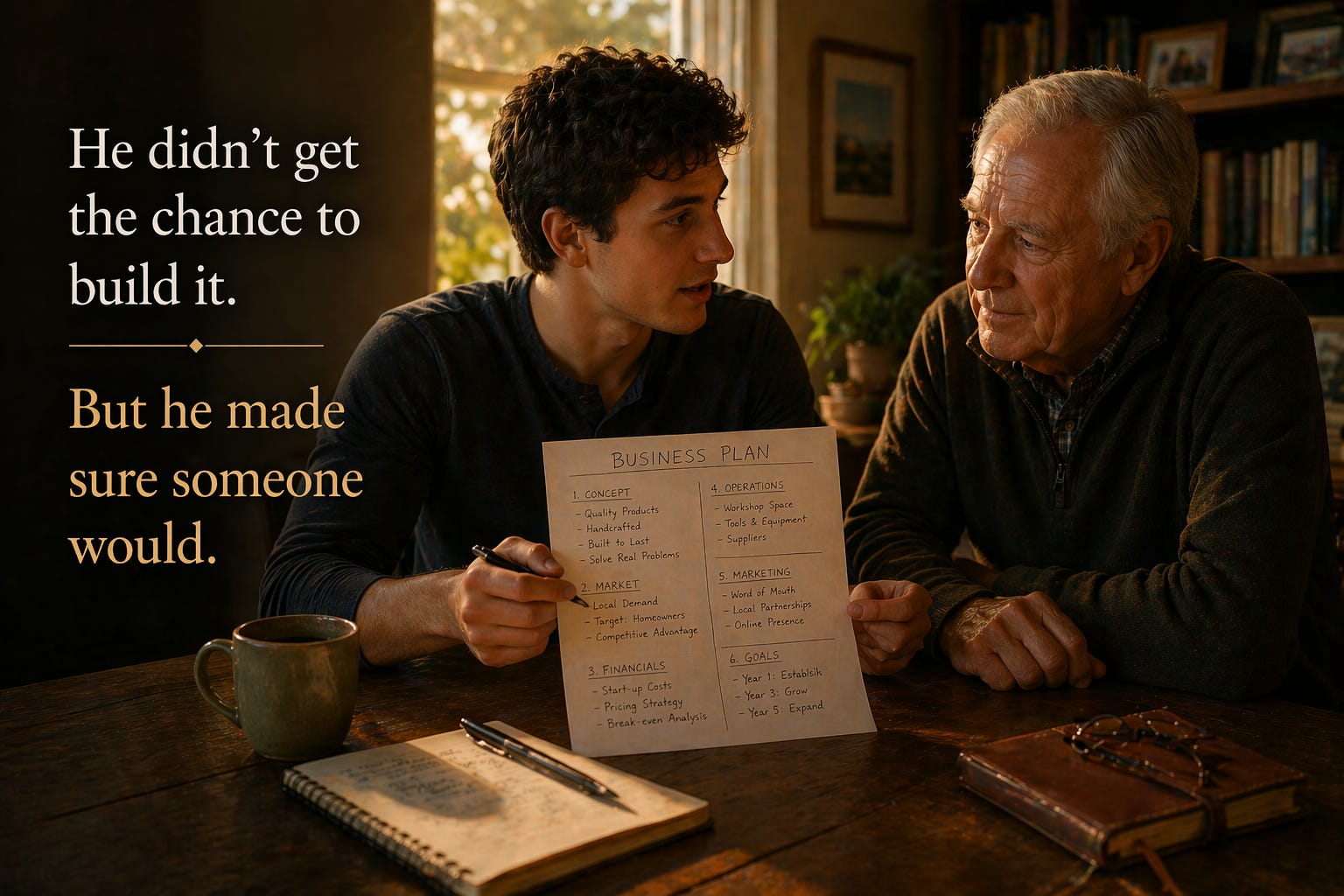

He came to me in his late sixties, recently retired, with a rollover IRA and a pension that covered his expenses comfortably. His grandson had just told him about a business idea. Good idea, he said. Solid market. The kid had done the research.

What he needed was a start.

“I want to make sure that never stops a good idea in this family again,” he told me. “Not for him, and not for anyone who comes after him.”

What he was describing has a name most families have never heard applied to themselves. An endowment.

Universities and foundations use them to fund programs in perpetuity. The mechanism is the same regardless of the purpose: a sum of money goes into an investment account, only the growth is ever spent, and the principal compounds forever. The gift never runs out because the source is never touched.

Most families have never built one not because they lacked the resources but because nobody ever told them they could. A grandfather with a $50,000 account he no longer needs can build a permanent family venture fund using exactly the same structure that institutions have used for generations.

The seed amount does not have to be large. It has to be structured correctly.

The legal vehicle that makes this permanent is a trust. Not a savings account, not a brokerage account, not a verbal agreement between family members. A trust is a legal entity that owns the money independently of any individual. It survives the person who created it, operates according to written instructions that cannot be casually overridden, and protects the assets from probate, from creditors, and from the kind of informal family decisions that drain inherited money before it reaches the people it was meant for. The endowment mechanism only works permanently because the trust makes it permanent. Without the trust, the structure is a good intention. With it, it is a binding plan.

Here is what the structure looks like.

The $50,000 goes into a trust-owned investment account. The trust owns the money, not the grandchildren, not the future entrepreneurs, which protects it from probate, from disputes, and from the kind of well-meaning decisions that drain inherited money before it reaches the people it was meant for.

The trust has one instruction: use only the growth. Never touch the principal.

The trust document also specifies who qualifies, what they must provide to access the fund, how much they can receive, and what happens when the trustee changes over time. Every one of those decisions is made once, by the person who creates the trust, with the benefit of knowing the full picture. Future generations do not renegotiate the terms. They operate within them. That is what makes the structure last.

This endowment is structured with a higher growth threshold than a wedding or tool set fund, because the draw amounts are larger and the stakes of the investment are different. Rather than drawing as soon as the annual growth covers the contribution, this trust is designed to compound without draws until the account reaches a target size large enough to fund multiple business attempts across generations without straining the base.

The trust specifies exactly what qualifies for a draw: a legitimately registered business with a completed business plan, submitted to the trustee for review. Not an idea on a napkin. A registered entity with a documented plan. The bar is meaningful but not prohibitive. Its purpose is to ensure the capital goes to family members who are genuinely ready to build something, not to test whether they deserve the opportunity.

One additional clause many families include: each family member may access the fund once. If the business does not succeed, the experience was funded and the lesson was real. The fund is available to the next family member ready to try, not recycled back to the same person indefinitely.

The business starter endowment requires patience in the compounding phase that a smaller-draw fund does not. A car endowment or a tool set fund draws modest amounts regularly and reaches self-sustaining growth relatively quickly. A business starter fund draws larger amounts less frequently, which means the compounding window before the first draw needs to be longer. The trust is built to wait.

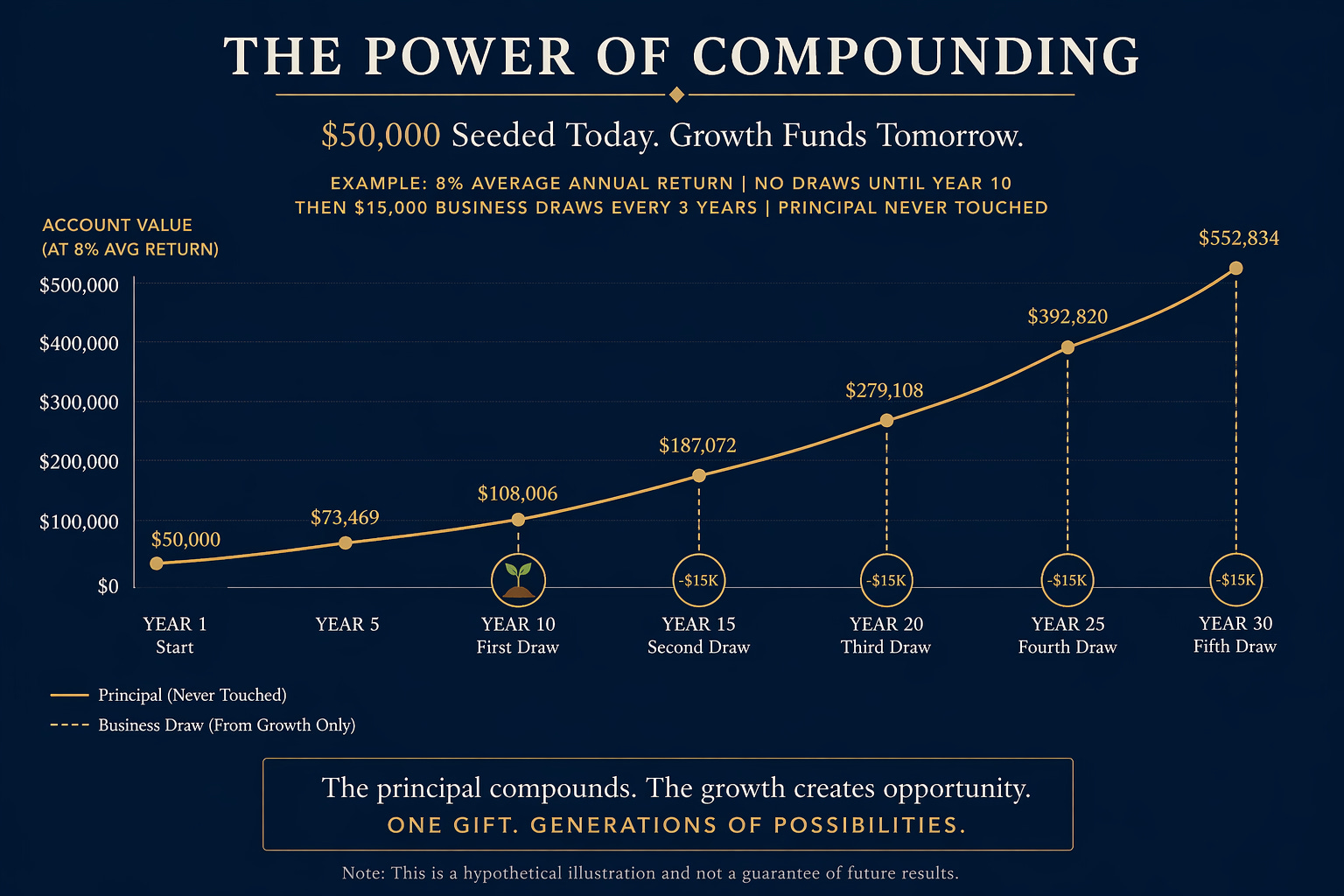

A $50,000 seed at 7 percent annual growth:

In year one, the account earns $3,500. The trust is not ready to fund a business start yet. The principal is still building toward the target threshold.

By year ten, the account has grown to $98,000. Annual growth exceeds $6,800. The trust is approaching the threshold where a meaningful first draw is available without reducing the compounding base significantly.

By year fifteen, the principal sits at $138,000. Annual growth exceeds $9,600. A business seed contribution of $15,000 to $20,000 is now available from accumulated growth, with the principal still intact and still compounding. That $15,000 is the same amount that was not there at twenty-two. The trust produces it from interest, every year, without reducing what comes next.

By year twenty, the account has reached $193,000. Annual growth exceeds $13,500. The fund can support multiple business starts per decade from growth alone, with the principal growing larger between draws rather than shrinking.

By year thirty, the account sits at $381,000. Annual growth exceeds $26,000. At that point the family venture fund is producing enough annual growth to seed two or three serious business starts per year without touching the founding principal.

The $50,000 he set aside never gets spent. Every business it funds is started from interest, not from principal. The next entrepreneur in the family line does not reduce what is available to the one who follows.

What happens when a family member’s business fails?

It happens. Most first businesses do not succeed, and anyone who has built something knows this. The trust is not designed to fund only winning ideas. It is designed to fund serious attempts by family members who are ready to try.

The loss of a draw does not damage the principal. The growth that funded the attempt was already produced by the account. The principal continues compounding. The next family member who qualifies for a draw accesses the next cycle of growth.

What the trust does is remove the most common reason good ideas never become businesses: not lack of ability, not lack of market, but lack of starting capital at the moment someone is ready to move.

Most family businesses fail in the first generation not because the ideas were bad but because the capital was not there when the window was open. An idea at twenty-two does not wait for a bank to approve a loan or a family member to liquidate savings. It either gets started or it does not. The window is open and then it closes.

This trust keeps the window open for every generation.

This is what The Legacy Blueprint is built around. Structures that solve the problems that stop families from building what they are capable of building. Subscribe free and get every post delivered to your inbox.

The money is not really the point.

What gets transmitted through a structure like this is a family culture that takes entrepreneurship seriously. Not as a gamble, not as a dream for the unusually talented, but as a legitimate path that this family supports structurally. Every family member who grows up knowing the fund exists approaches the question of starting a business differently. The question is not whether the capital will be there. The capital will be there. The question is whether the idea and the readiness are there.

That shift in the baseline question changes who tries.

Most people who never start a business will give you a reason that sounds like character: I was not ready, I was not sure enough, I did not think I had what it takes. Underneath most of those reasons is a simpler one. The risk was too high and the safety net was too thin. A first-generation entrepreneur with no family capital behind them is not just risking a business. They are risking their rent, their savings, their family’s stability. That is a different kind of risk than a person takes who knows that a failed attempt does not mean financial collapse.

The trust does not eliminate risk. It calibrates it. A family member who draws from the fund and fails has lost a business attempt. They have not lost everything. That difference is what allows more people in a family to try, and more attempts is how more successes happen.

He did not get to try at twenty-two. His grandson will. So will every entrepreneur who comes after in that family line, in businesses not yet imagined, in markets not yet formed, with ideas that do not exist yet.

The seed he planted will still be producing when the planters are long gone.

If you have a retirement account, a life insurance policy, or a savings balance sitting unused, this kind of structure may be the most productive thing it ever does. The Estate Planning Blueprint Masterclass walks through exactly how to set up a trust like this: what type of trust fits this structure, how to fund it with an existing account, how to write the instructions so they hold up across generations, and how to name a trustee who will carry the plan forward. This is the conversation most families never have because nobody put it in front of them clearly.

Register for the Free Estate Planning Blueprint Masterclass

https://lastinglegacypro.com/webinar

If you are ready to talk through what this looks like for your family:

Schedule Your Free Consultation

https://lastinglegacypro.com/consultation

The idea that never got started because the capital was not there is still in your family line. The next one does not have to wait.

Nathaniel Vale The Legacy Blueprint

Thanks for reading The Legacy Blueprint. If this resonated with you or someone in your family has ever had a good idea and not enough to start, subscribe free. A new piece like this lands in your inbox every week.