Debts Don't Inherit. Family Members Often Pay Them Anyway.

The priority order family members never see, and the four decisions that quietly turn structural protection into personal liability.

The Hidden Truths series Post 04

The Hidden Truths examines the gap between what families believe their estate plan will do and what the legal system actually does after a death. Each post follows one family through one specific failure that planning could have prevented.

There is a common belief, repeated at family dinners and funerals across the country, that when a person dies, their debts die with them. The belief is partially right and dangerously incomplete. Most families do not legally inherit a deceased relative’s debts, yet many family members end up paying them anyway. Four specific situations during the weeks after a death account for most of those payments, and this post examines each one.

The right part is that family does not inherit the deceased’s debts. A son does not become responsible for his late father’s credit cards. A sister does not inherit her late brother’s medical bills. A niece does not pick up the unpaid taxes of an aunt. None of these debts are automatically transferred to family members by virtue of family relationship.

The dangerously incomplete part is that the debts do not simply disappear. They survive the debtor as claims against the estate, and the estate distributes the deceased’s assets in a fixed legal order to satisfy them. The will does not change the order. A revocable living trust does not change the order; in Arizona and in nearly every other state, the assets of a revocable trust become reachable by the settlor’s creditors after death. The order is procedural, applies regardless of how the deceased held their property, and in nearly every jurisdiction places the family in the same position.

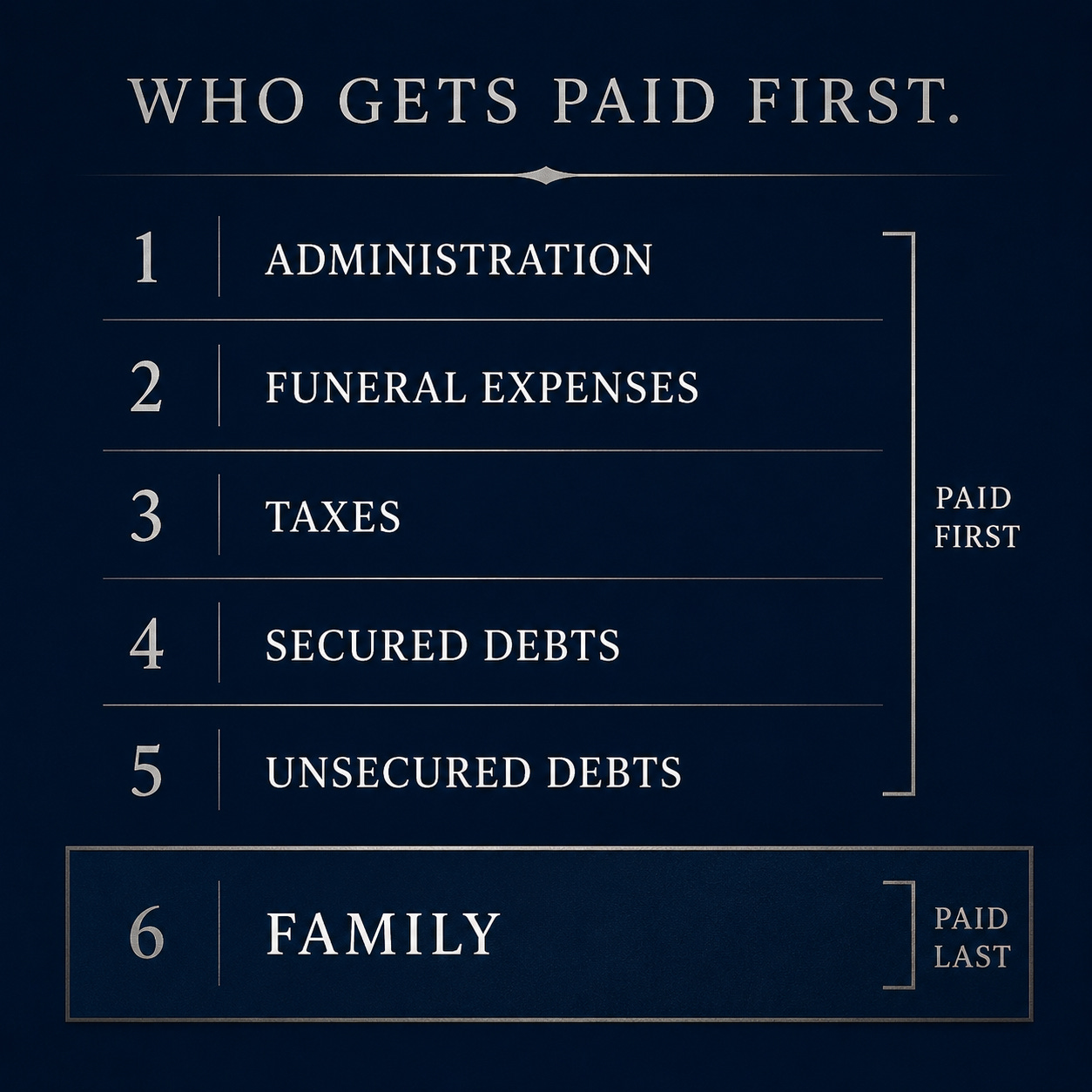

Family is sixth.

The order itself

The five tiers ahead of family are these.

Administration costs come first. Probate court fees, the executor’s compensation, the estate’s attorney, the appraiser, the accountant. These costs come off the top of the estate before anyone else receives anything.

Funeral expenses come second, capped at what the court considers reasonable.

Tax obligations come third. Federal and state income tax, property tax, any estate tax that applies. Tax claims are senior to nearly every private debt.

Secured debts come fourth. Mortgages, auto loans, equipment financing, anything backed by specific collateral.

Unsecured debts come fifth. Credit card balances, medical bills, personal loans, anything without collateral attached.

Family is sixth. Whatever survives the first five tiers is what flows to heirs. If the first five tiers consume the entire estate, the family receives nothing. If the first five tiers fail to consume the entire estate, family receives the residual.

This is the priority order that decides what an estate actually delivers, regardless of what the will says.

What the family owes when the estate cannot pay

The part most families do not understand, and the part that matters most for the family member who is handling the final affairs, is this: when the estate runs out of assets, family is not pulled forward to make up the difference. The unpaid creditors absorb the loss. The family member is not personally liable for the deceased’s solo debts, even when the estate cannot cover them.

That is the default legal position of family. The estate is the proper repository for the deceased’s obligations. Family stands adjacent to the estate, not inside it. The system processes the estate. Family is processed by no one.

There is one structural exception. Debts that bear the family member’s name as a co-signer or joint borrower are not solo debts of the deceased. They are debts of two or more obligors, and the family member who signed remains liable when the other obligor dies. A parent who co-signed a child’s student loan remains liable after the child dies. A spouse on a joint credit card remains liable for the balance even if the spouse never made a single purchase. An adult child who co-signed on an aging parent’s auto loan or apartment lease remains personally liable when the parent dies. These obligations bypass the priority order entirely because the surviving obligor is a faster path to recovery than the estate.

The family pays only what the family signed for. That is the default. Everything else flows through the estate and stops at the estate’s limits.

So why do so many family members end up paying the deceased’s solo debts anyway?

Because the default protection can be voluntarily surrendered, and four common situations during the weeks after a death produce that surrender. The protection is real. The pathways out of it are short, common, and rarely recognized in time.

The first trap: the funeral home

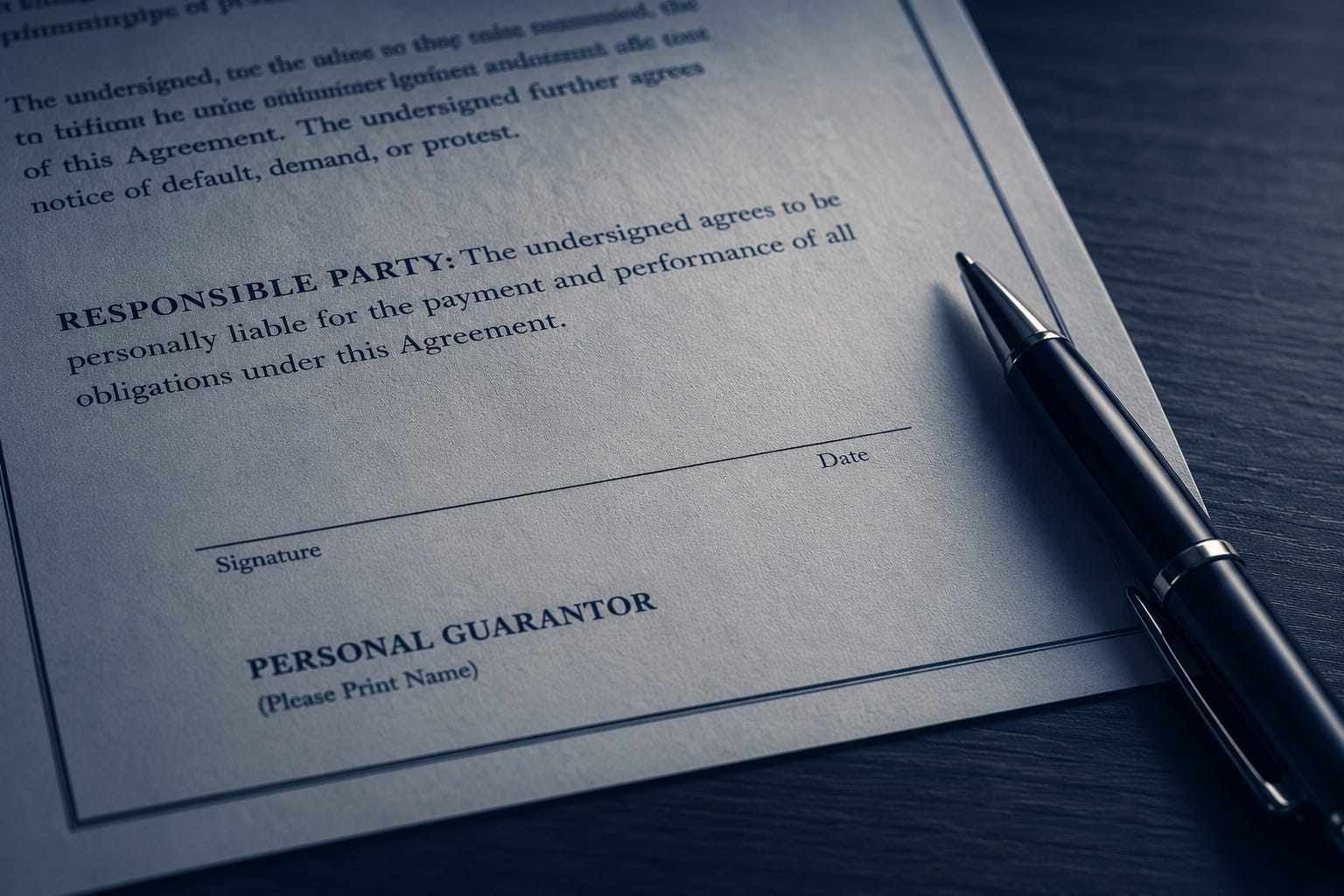

The first situation is the funeral home. When a family member walks into a funeral home to make arrangements, the funeral director presents a contract that includes a “responsible party” or “guarantor” signature line. The person who signs that line is personally guaranteeing payment of the funeral cost. The signature converts the funeral expense from an estate debt, which would otherwise be paid from estate assets in the second tier of the priority order, into a personal debt of the signer.

The funeral home asks for this signature because the funeral home knows the estate may be unable to pay. The contract is a credit transaction, and the personal guarantee is the funeral home’s protection against the estate’s insolvency. From the funeral home’s perspective, this is rational risk management. From the signer’s perspective, it is the conversion of a non-obligation into an obligation, often within forty-eight hours of the death, signed during acute grief, almost never read carefully.

The counter-move is to sign only as representative of the estate, not as personal guarantor. This requires the signer to ask the funeral director to amend the signature line or to mark the signature “as representative of the estate of [name], not personally.” Some funeral homes will accommodate this. Some will not, and will require a personal guarantee as a condition of service.

When personal guarantee is required and cannot be removed from the contract, the family member has three viable paths. The first is to pay the funeral cost in advance from the estate’s available liquid assets, eliminating the credit element of the transaction. The second is to choose a direct cremation provider, many of which do not require personal guarantees and which can deliver remains for under $1,500 nationally. The third is to sign the personal guarantee with full awareness that the cost will become personal debt regardless of what the estate can pay, and to budget accordingly.

The most common path through this trap is the path of least resistance: a full traditional funeral arrangement, signed for personally, costing between $8,000 and $15,000, with the signer responsible for the gap between what the estate can pay and the full amount. This is also the most expensive path, and it is the path the funeral industry’s contract structure is designed to produce.

The second trap: debt collectors

The second situation is the debt collector. Within weeks of a death, the deceased’s creditors begin contacting the family. The contact comes through phone calls to numbers found through public records, letters to the deceased’s last known address, and increasingly, messages to family members identified through social media or court filings.

The language used by collectors is designed to imply liability that does not exist. Common phrases include “as the executor you are now responsible for these accounts,” “your loved one’s debts are now your responsibility,” and “the family needs to take care of this before the estate can close.” None of these statements is legally accurate. The executor’s responsibility is to administer the estate according to the priority order, not to personally pay the estate’s debts. A family member who is not on the original debt as a co-signer or joint borrower has no personal liability for the debt, regardless of the role they play in handling the deceased’s affairs.

Collectors use this language because it works. A meaningful percentage of family members who receive these calls end up paying some portion of the debt, often from their own funds, under the belief that they are legally required to. The Consumer Financial Protection Bureau and the Federal Trade Commission have both published guidance documenting the pattern.

The counter-move has two parts. First, the family member sends the collector written notice that the family member is not personally liable for the debt and that all future communication regarding the debt must be directed to the estate, if probate has been opened, or otherwise must cease. Under the Fair Debt Collection Practices Act, collectors are required to honor written cease-communication requests from non-debtors. Second, the family member does not engage in verbal arguments with the collector about the merits. There is no productive conversation to be had. The collector’s role is to extract payment. The family member’s role is to refuse the extraction.

If probate is open, the collector should file a formal claim with the personal representative within the claims window. If probate is not open and the estate has no recoverable assets, the collector has no path to recover the debt and will eventually write it off.

The third trap: voluntary payment

The third situation is voluntary payment. Some family members, after enough collector pressure or out of a sense of duty to the deceased, decide to pay the deceased’s debts personally. The payment is sometimes framed as honoring the deceased’s intentions, sometimes as protecting the deceased’s credit reputation, sometimes simply as making the collectors stop calling.

None of these reasons creates a legal obligation. The deceased’s intentions do not transfer to a family member through grief alone. The deceased’s credit reputation no longer matters once the credit accounts are closed by death. The collectors will stop calling once the family member tells them in writing to stop.

A family member who pays the deceased’s solo debt with their own money has converted a non-debt into a payment they cannot recover. The estate cannot reimburse them, because the estate does not owe them anything. The deceased’s heirs cannot reimburse them, because the heirs received whatever they received separately. The money is simply gone.

The counter-move is to recognize that “honoring the deceased” and “personally paying the deceased’s debts” are different actions, and the law does not equate them. Family members who want to express their commitment to the deceased’s memory have many ways to do so. Paying a credit card balance to a corporation that has already absorbed the loss into its bad-debt accounting is not one of the meaningful ones.

The exception worth naming, again, is the co-signed debt. A debt the family member signed remains the family member’s obligation, separate from the deceased and separate from the estate. Paying that debt is not voluntary in the same sense; it is paying what the family member already owes.

The fourth trap: the personal representative role

The fourth situation is the personal representative role itself. When a family member accepts appointment as personal representative (executor named in the will, or administrator appointed by the court when there is no will), they take on a fiduciary duty to administer the estate according to law. The duty includes inventorying assets, notifying creditors, paying claims in priority order, and distributing whatever remains to heirs.

The trap inside this duty is the possibility of doing it wrong. A personal representative who distributes estate assets to heirs before paying creditors in the priority order can become personally liable to those creditors for the value distributed. The same applies to a personal representative who closes the estate without satisfying valid claims, who fails to file required inventories or accountings, or who takes personal property from the estate without proper distribution. Creditors who receive less than they would have under proper administration can sue the personal representative individually. Heirs who receive less than they should have can also sue.

This is not a theoretical exposure. Fiduciary liability is the most common way family members who took the personal representative role specifically to “help out” end up paying for the estate’s shortfalls with their own money.

The counter-move is one of three paths. The first is to decline the appointment. Personal representative service is not mandatory, and the court will appoint a successor or a public administrator if no family member accepts. The second path, for family members who do take the role, is to retain an attorney to guide the administration. The attorney’s fee is paid from the estate, in the first tier of the priority order, before any creditor or heir receives anything; the personal representative does not pay the attorney out of pocket. The third path, for estates with truly limited assets, is to not open probate at all. Arizona and most other states have small estate procedures that allow heirs to claim limited personal property through affidavit without opening formal probate. If no probate is opened, no personal representative is appointed, no fiduciary duty attaches, and the question of personal liability for administration errors does not arise. The creditors of an insolvent estate that is never probated will eventually write the debts off.

What the family is being asked, in each trap

The four traps share a common shape. In each one, an institution or a feeling presents the family member with an opportunity to step out of the structural protection the law has placed them inside.

The funeral home presents the opportunity as a signature line at the bottom of a contract.

The debt collector presents the opportunity as a verbal claim of liability that does not exist.

The family member’s own sense of duty presents the opportunity as a payment made to honor the deceased.

The personal representative role presents the opportunity as a fiduciary error.

In each case, the family member begins outside the line and ends inside it. The institutional actor on the other side of each interaction is sophisticated and has run the play many times before. The family member is grieving, exhausted, and is encountering each play for the first time.

The structural protection family members have against a deceased relative’s debts is real. It is created by the priority order, by the legal separation between the deceased’s obligations and the family member’s personal finances, and by the limits of what the estate can pay. The protection is also fragile. It is the default, and the default holds only as long as the family member does not voluntarily step outside it.

The will tells the estate what the deceased wanted. The priority order tells the estate what it must do. Neither of those documents requires the family to pay anything. The family pays only what the family signed for, and only what the family chooses to surrender.

This post described the priority order that processes a deceased person's debts and the four traps that quietly pull family members into paying debts they never owed. The work that prevents both, and that keeps more of an estate outside the priority order entirely, happens earlier, when the estate plan is built. The Estate Planning Blueprint Masterclass is a free one-hour class for families who want to build an estate plan that holds up. It walks through the three things every plan needs to keep probate out, protect children from avoidable conflict, and pass wealth to the next generation cleanly. Readers who recognized the patterns in this post and want to start building the structure that prevents them can register here:

Register for the Masterclass

Readers who would prefer to discuss a specific situation directly can book a free consultation here: